Trending in Quantitative Finance

Deep Learning for Financial Time Series: A Large-Scale Benchmark of Risk-Adjusted Performance

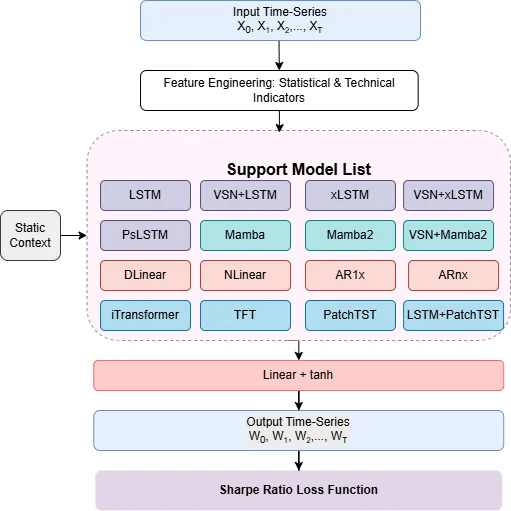

We present a large scale benchmark of modern deep learning architectures for a financial time series prediction and position sizing task, with a primary focus on Sharpe ratio optimization. Evaluating linear models, recurrent networks, transformer based architectures, state space models, and recent sequence representation approaches, we assess out of sample performance on a daily futures dataset spanning commodities, equity indices, bonds, and FX spanning 2010 to 2025. Our evaluation goes beyond average returns and includes statistical significance, downside and tail risk measures, breakeven transaction cost analysis, robustness to random seed selection, and computational efficiency. We find that models explicitly designed to learn rich temporal representations consistently outperform linear benchmarks and generic deep learning models, which often lead the ranking in standard time series benchmarks. Hybrid models such as VSN with LSTM, a combination of Variable Selection Networks (VSN) and LSTMs, achieves the highest overall Sharpe ratio, while VSN with xLSTM and LSTM with PatchTST exhibit superior downside adjusted characteristics. xLSTM demonstrates the largest breakeven transaction cost buffer, indicating improved robustness to trading frictions.

2603.01820

Mar 2026Trading and Market Microstructure

QuantaAlpha: An Evolutionary Framework for LLM-Driven Alpha Mining

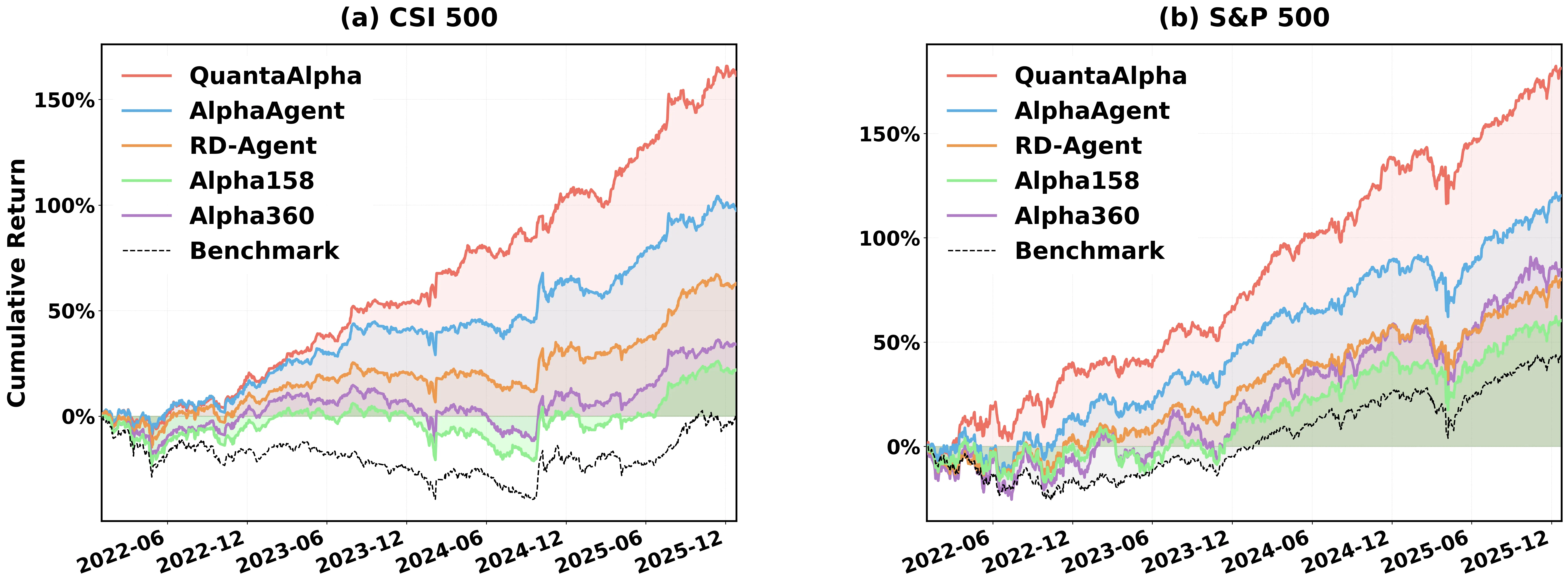

Financial markets are noisy and non-stationary, making alpha mining highly sensitive to noise in backtesting results and sudden market regime shifts. While recent agentic frameworks improve alpha mining automation, they often lack controllable multi-round search and reliable reuse of validated experience. To address these challenges, we propose QuantaAlpha, an evolutionary alpha mining framework that treats each end-to-end mining run as a trajectory and improves factors through trajectory-level mutation and crossover operations. QuantaAlpha localizes suboptimal steps in each trajectory for targeted revision and recombines complementary high-reward segments to reuse effective patterns, enabling structured exploration and refinement across mining iterations. During factor generation, QuantaAlpha enforces semantic consistency across the hypothesis, factor expression, and executable code, while constraining the complexity and redundancy of the generated factor to mitigate crowding. Extensive experiments on the China Securities Index 300 (CSI 300) demonstrate consistent gains over strong baseline models and prior agentic systems. When utilizing GPT-5.2, QuantaAlpha achieves an Information Coefficient (IC) of 0.1501, with an Annualized Rate of Return (ARR) of 27.75% and a Maximum Drawdown (MDD) of 7.98%. Moreover, factors mined on CSI 300 transfer effectively to the China Securities Index 500 (CSI 500) and the Standard & Poor's 500 Index (S&P 500), delivering 160% and 137% cumulative excess return over four years, respectively, which indicates strong robustness of QuantaAlpha under market distribution shifts.

2602.07085

Feb 2026Statistical Finance

Uncertainty-Adjusted Sorting for Asset Pricing with Machine Learning

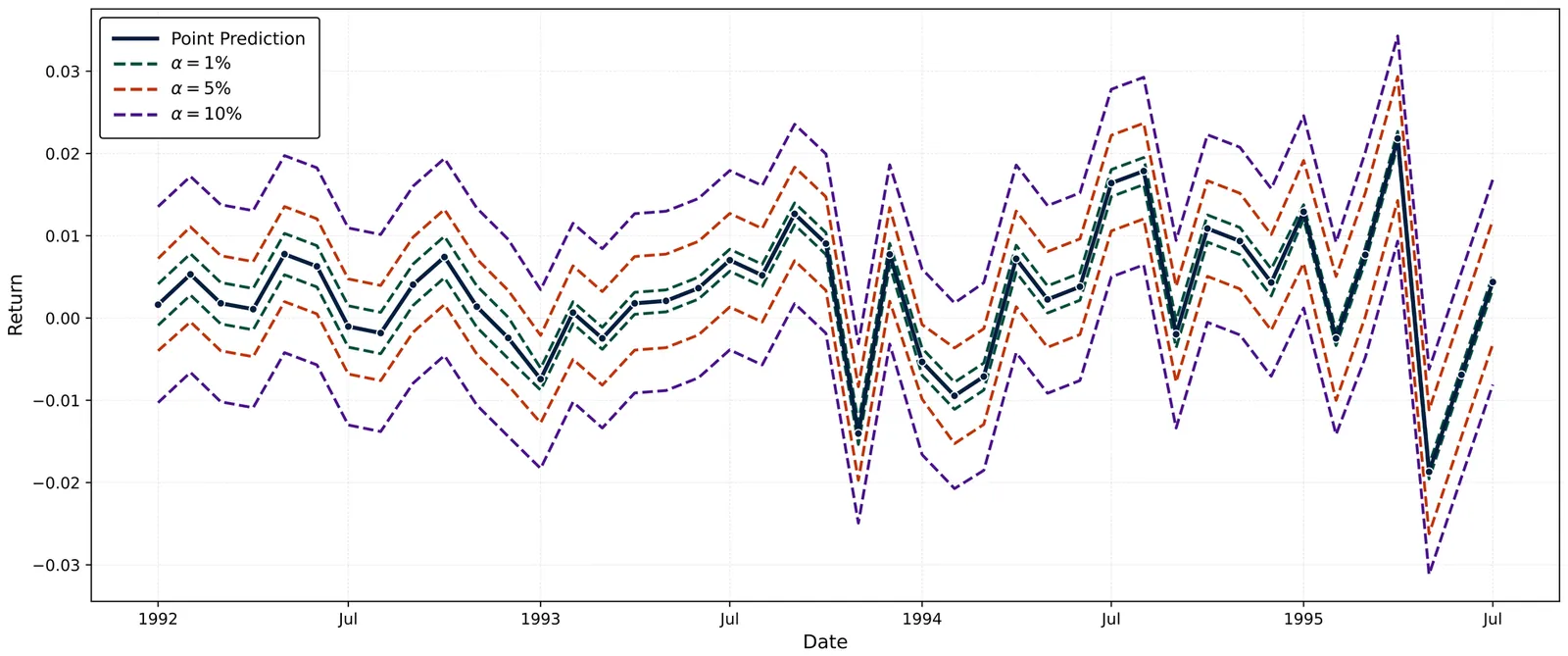

Machine learning is central to empirical asset pricing, but portfolio construction still relies on point predictions and largely ignores asset-specific estimation uncertainty. We propose a simple change: sort assets using uncertainty-adjusted prediction bounds instead of point predictions alone. Across a broad set of ML models and a U.S. equity panel, this approach improves portfolio performance relative to point-prediction sorting. These gains persist even when bounds are built from partial or misspecified uncertainty information. They arise mainly from reduced volatility and are strongest for flexible machine learning models. Identification and robustness exercises show that these improvements are driven by asset-level rather than time or aggregate predictive uncertainty.

2601.00593

Jan 2026Portfolio Management

Alpha-R1: Alpha Screening with LLM Reasoning via Reinforcement Learning

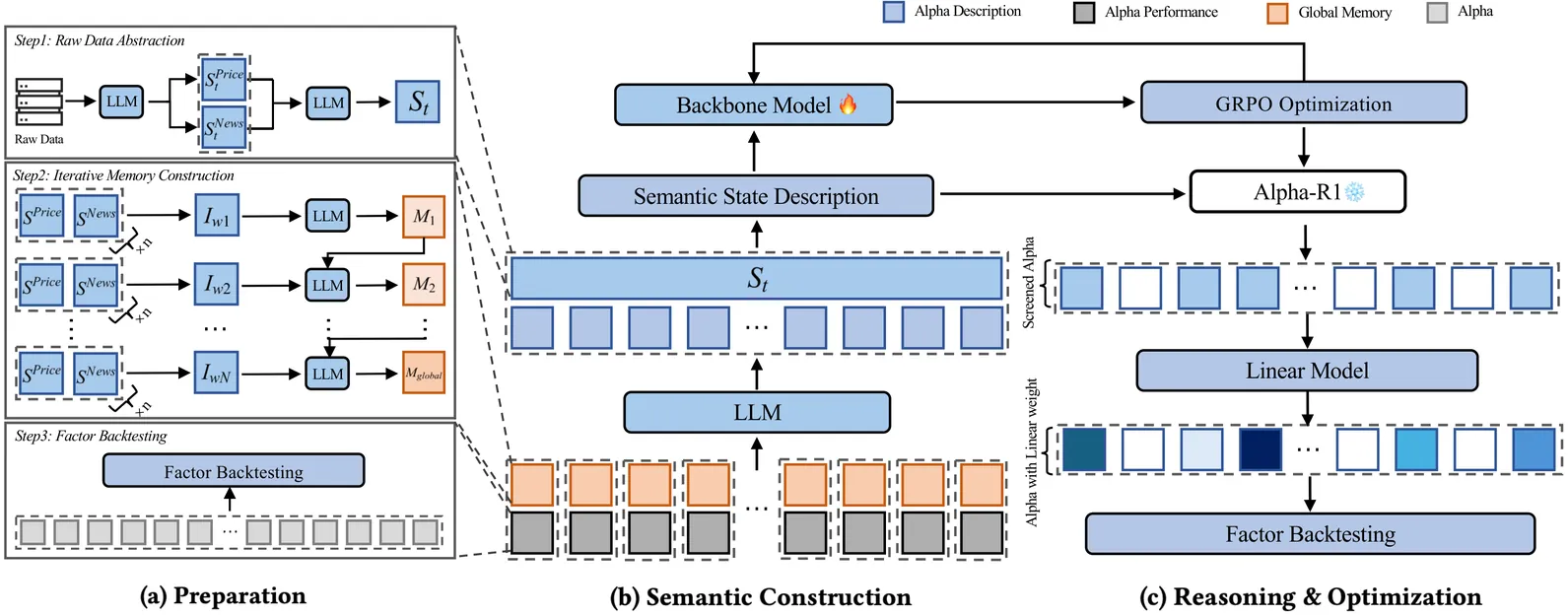

Signal decay and regime shifts pose recurring challenges for data-driven investment strategies in non-stationary markets. Conventional time-series and machine learning approaches, which rely primarily on historical correlations, often struggle to generalize when the economic environment changes. While large language models (LLMs) offer strong capabilities for processing unstructured information, their potential to support quantitative factor screening through explicit economic reasoning remains underexplored. Existing factor-based methods typically reduce alphas to numerical time series, overlooking the semantic rationale that determines when a factor is economically relevant. We propose Alpha-R1, an 8B-parameter reasoning model trained via reinforcement learning for context-aware alpha screening. Alpha-R1 reasons over factor logic and real-time news to evaluate alpha relevance under changing market conditions, selectively activating or deactivating factors based on contextual consistency. Empirical results across multiple asset pools show that Alpha-R1 consistently outperforms benchmark strategies and exhibits improved robustness to alpha decay. The full implementation and resources are available at https://github.com/FinStep-AI/Alpha-R1.

2512.23515

Dec 2025Trading and Market Microstructure

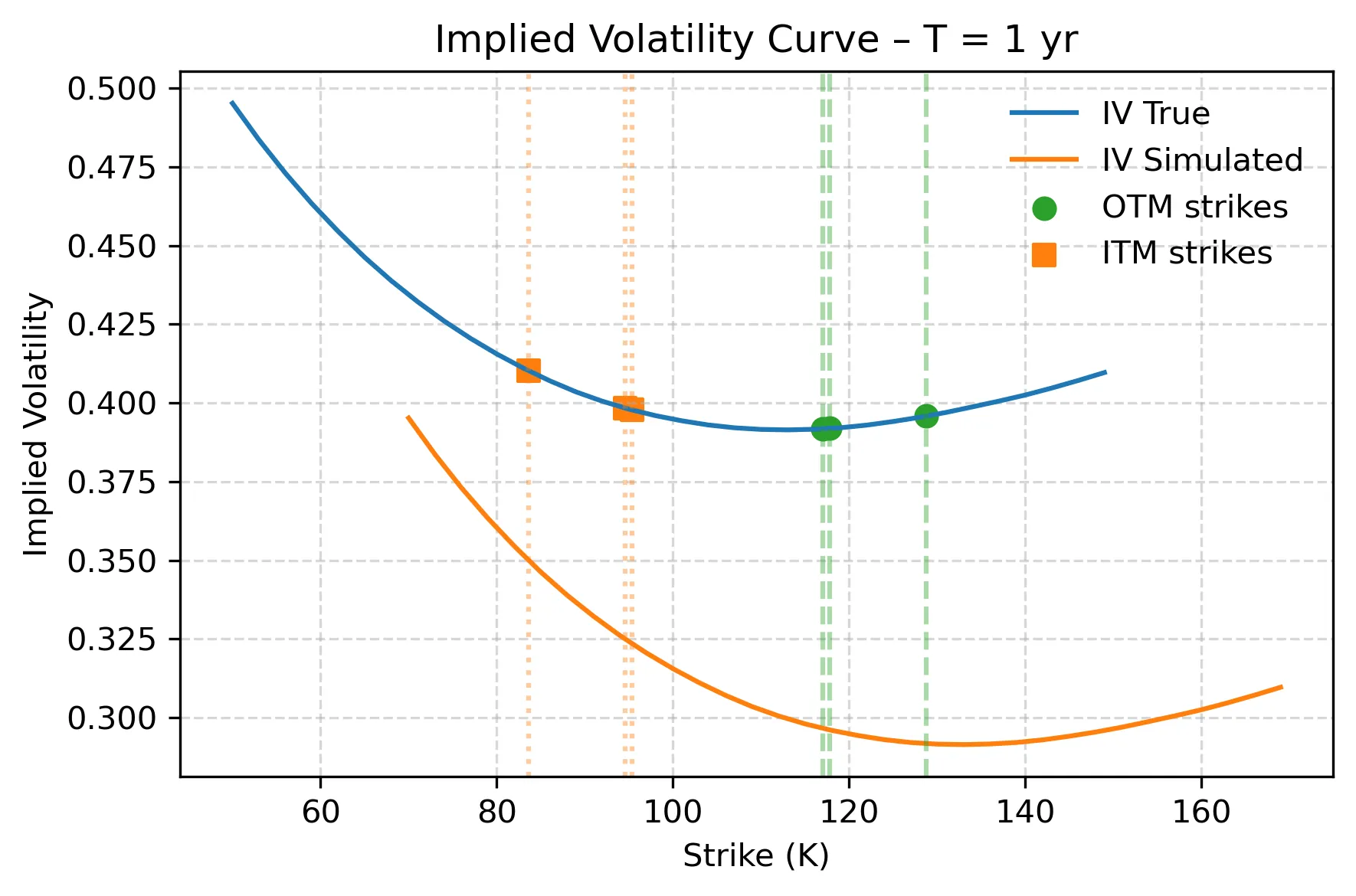

Transfer Learning (Il)liquidity

The estimation of the Risk Neutral Density (RND) implicit in option prices is challenging, especially in illiquid markets. We introduce the Deep Log-Sum-Exp Neural Network, an architecture that leverages Deep and Transfer learning to address RND estimation in the presence of irregular and illiquid strikes. We prove key statistical properties of the model and the consistency of the estimator. We illustrate the benefits of transfer learning to improve the estimation of the RND in severe illiquidity conditions through Monte Carlo simulations, and we test it empirically on SPX data, comparing it with popular estimation methods. Overall, our framework shows recovery of the RND in conditions of extreme illiquidity with as few as three option quotes.

2512.11731

Dec 2025Mathematical Finance

Arbitrage-Free Option Price Surfaces via Chebyshev Tensor Bases and a Hamiltonian Fog Post-Fit

We study the construction of arbitrage-free option price surfaces from noisy bid-ask quotes across strike and maturity. Our starting point is a Chebyshev representation of the call price surface on a warped log-moneyness/maturity rectangle, together with linear sampling and no-arbitrage operators acting on a collocation grid. Static no-arbitrage requirements are enforced as linear inequalities, while the surface is fitted directly to prices via a coverage-seeking quadratic objective that trades off squared band misfit against spectral and transport-inspired regularisation of the Chebyshev coefficients. This yields a strictly convex quadratic program in the modal coefficients, solvable at practical scales with off-the-shelf solvers (OSQP). On top of the global backbone, we introduce a local post-fit layer based on a discrete fog of risk-neutral densities on a three-dimensional lattice (m,t,u) and an associated Hamiltonian-type energy. On each patch of the (m,t) plane, the fog variables are coupled to a nodal price field obtained from the baseline surface, yielding a joint convex optimisation problem that reweights noisy quotes and applies noise-aware local corrections while preserving global static no-arbitrage and locality. The method is designed such that for equity options panels, the combined procedure achieves high inside-spread coverage in stable regimes (in calm years, 98-99% of quotes are priced inside the bid-ask intervals) and low rates of static no-arbitrage violations (below 1%). In stressed periods, the fog layer provides a mechanism for controlled leakage outside the band: when local quotes are mutually inconsistent or unusually noisy, the optimiser allocates fog mass outside the bid-ask tube and justifies small out-of-band deviations of the post-fit surface, while preserving a globally arbitrage-free and well-regularised description of the option surface.

2512.01967

Dec 2025Mathematical Finance