Mathematical Finance

arXiv:q-fin.MF

Mathematical and stochastic analysis of financial markets, derivative pricing and hedging.

Looking for a broader view? This category is part of:

Mathematical and stochastic analysis of financial markets, derivative pricing and hedging.

Looking for a broader view? This category is part of:

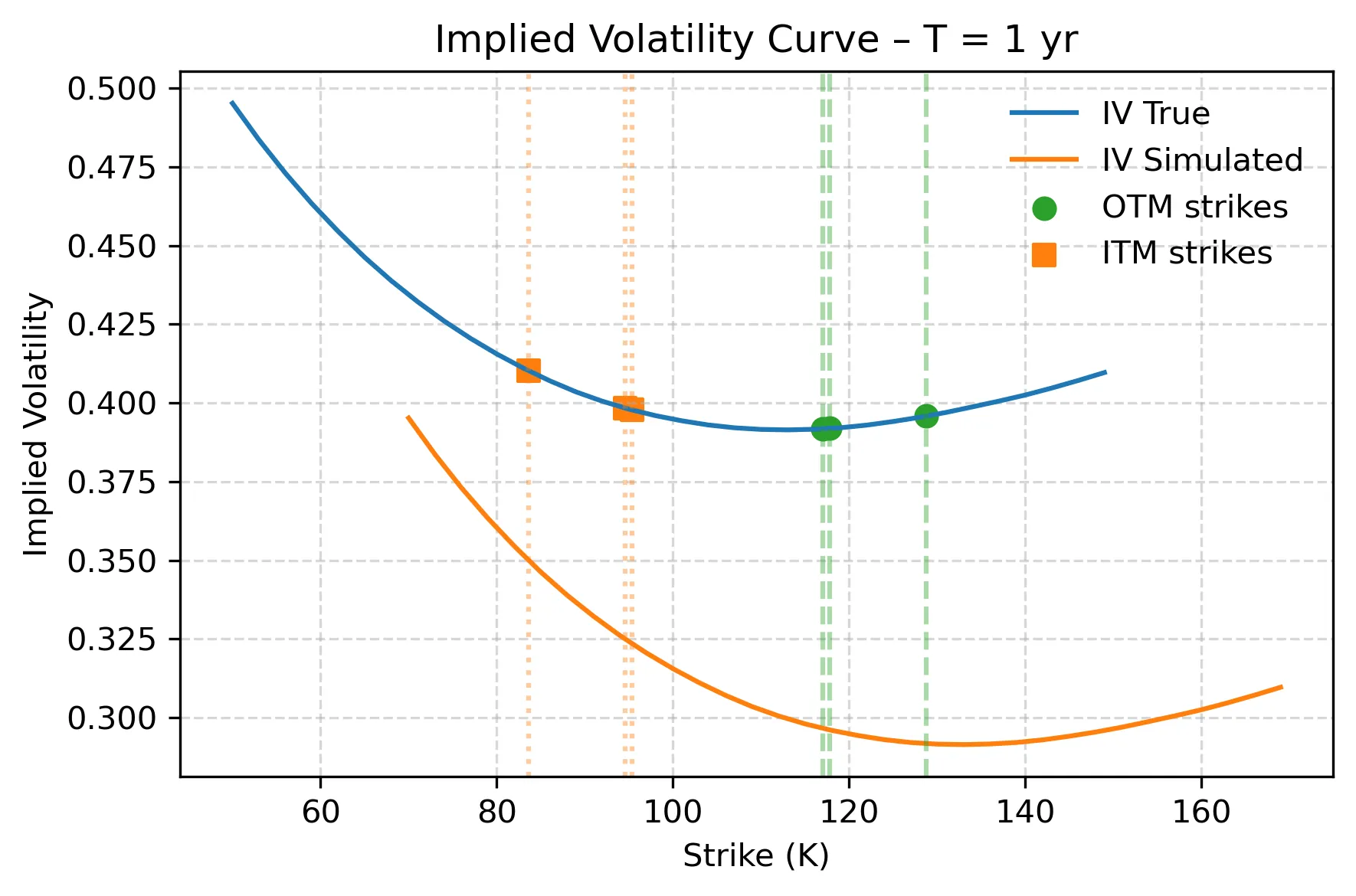

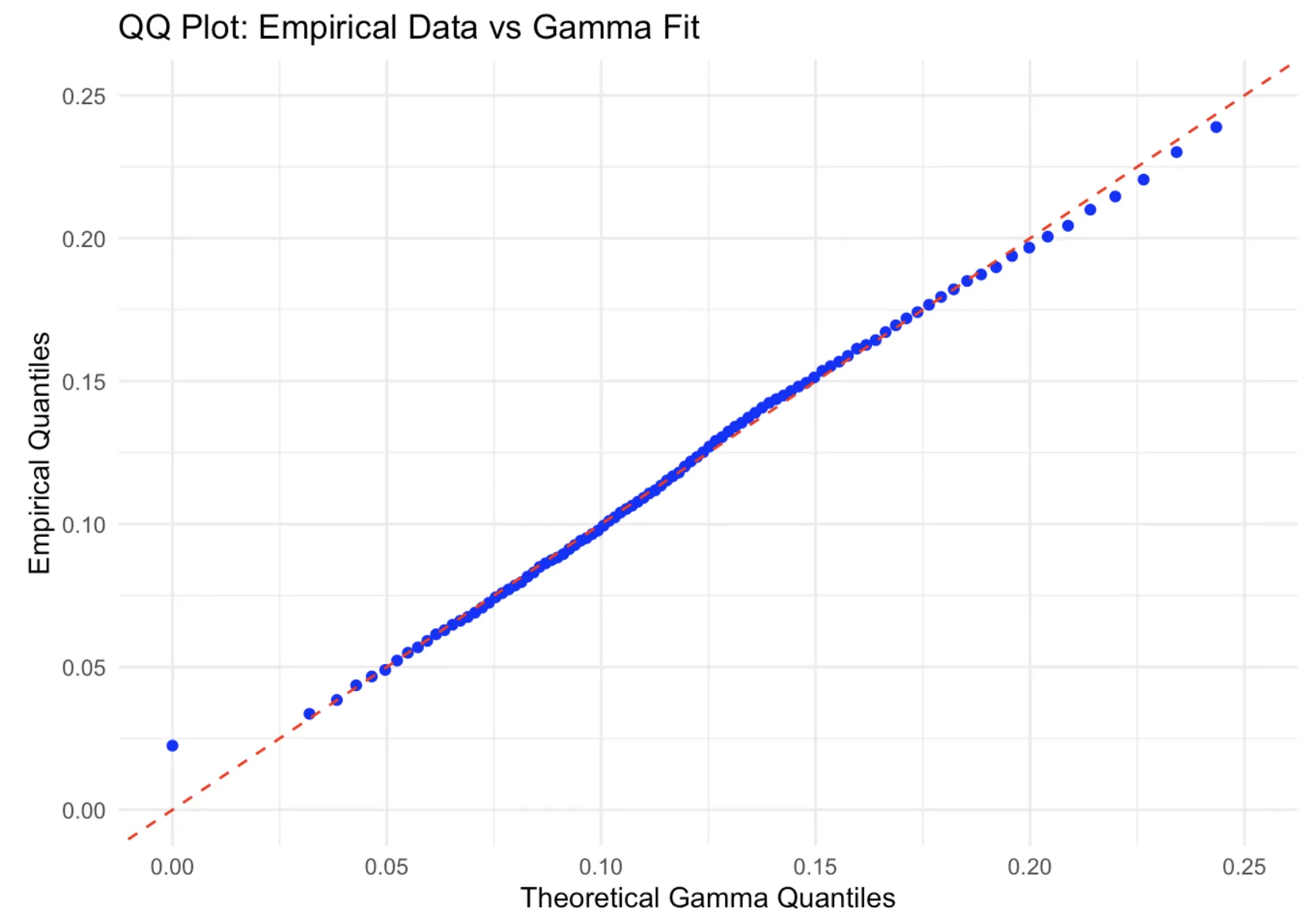

The estimation of the Risk Neutral Density (RND) implicit in option prices is challenging, especially in illiquid markets. We introduce the Deep Log-Sum-Exp Neural Network, an architecture that leverages Deep and Transfer learning to address RND estimation in the presence of irregular and illiquid strikes. We prove key statistical properties of the model and the consistency of the estimator. We illustrate the benefits of transfer learning to improve the estimation of the RND in severe illiquidity conditions through Monte Carlo simulations, and we test it empirically on SPX data, comparing it with popular estimation methods. Overall, our framework shows recovery of the RND in conditions of extreme illiquidity with as few as three option quotes.

We study the construction of arbitrage-free option price surfaces from noisy bid-ask quotes across strike and maturity. Our starting point is a Chebyshev representation of the call price surface on a warped log-moneyness/maturity rectangle, together with linear sampling and no-arbitrage operators acting on a collocation grid. Static no-arbitrage requirements are enforced as linear inequalities, while the surface is fitted directly to prices via a coverage-seeking quadratic objective that trades off squared band misfit against spectral and transport-inspired regularisation of the Chebyshev coefficients. This yields a strictly convex quadratic program in the modal coefficients, solvable at practical scales with off-the-shelf solvers (OSQP). On top of the global backbone, we introduce a local post-fit layer based on a discrete fog of risk-neutral densities on a three-dimensional lattice (m,t,u) and an associated Hamiltonian-type energy. On each patch of the (m,t) plane, the fog variables are coupled to a nodal price field obtained from the baseline surface, yielding a joint convex optimisation problem that reweights noisy quotes and applies noise-aware local corrections while preserving global static no-arbitrage and locality. The method is designed such that for equity options panels, the combined procedure achieves high inside-spread coverage in stable regimes (in calm years, 98-99% of quotes are priced inside the bid-ask intervals) and low rates of static no-arbitrage violations (below 1%). In stressed periods, the fog layer provides a mechanism for controlled leakage outside the band: when local quotes are mutually inconsistent or unusually noisy, the optimiser allocates fog mass outside the bid-ask tube and justifies small out-of-band deviations of the post-fit surface, while preserving a globally arbitrage-free and well-regularised description of the option surface.

We study contagion and systemic risk in sparse financial networks with balance-sheet interactions on a directed random graph. Each institution has homogeneous liabilities and equity, and exposures along outgoing edges are split equally across counterparties. A linear fraction of institutions have zero out-degree in sparse digraphs; we adopt an external-liability convention that makes the exposure mapping well-defined without altering propagation. We isolate a single-hit transmission mechanism and encode it by a sender-truncated subgraph G_sh. We define adversarial and random systemic events with shock size k_n = c log n and systemic fraction epsilon n. In the subcritical regime rho_out < 1, we prove that maximal forward reachability in G_sh is O(log n) with high probability, yielding O((log n)^2) cascades from shocks of size k_n. For random shocks, we give an explicit fan-in accumulation bound, showing that multi-hit defaults are negligible with high probability when the explored default set is polylogarithmic. In the supercritical regime, we give an exact distributional representation of G_sh as an i.i.d.-outdegree random digraph with uniform destinations, placing it within the scope of the strong-giant/bow-tie theorem of Penrose (2014). We derive the resulting implication for random-shock systemic events. Finally, we explain why sharp-threshold machinery does not directly apply: systemic-event properties need not be monotone in the edge set because adding outgoing edges reduces per-edge exposure.

This article constructs a forward exponential utility in a market with multiple defaultable risks. Using the Jacod-Pham decomposition for random fields, we first characterize forward performance processes in a defaultable market under the default-free filtration. We then construct a forward utility via a system of recursively defined, indexed infinite-horizon backward stochastic differential equations (BSDEs) with discounting, and establish the existence, uniqueness, and boundedness of their solutions. To verify the required (super)martingale property of the performance process, we develop a rigorous characterization of this property with respect to the general filtration in terms of a set of (in)equalities relative to the default-free filtration. We further extend the analysis to a stochastic factor model with ergodic dynamics. In this setting, we derive uniform bounds for the Markovian solutions of the infinite-horizon BSDEs, overcoming technical challenges arising from the special structure of the system of BSDEs in the defaultable setting. Passing to the ergodic limit, we identify the limiting BSDE and relate its constant to the risk-sensitive long-run growth rate of the optimal wealth process.

We study non-linear Backward Stochastic Differential Equations (BSDEs) driven by a Brownian motion and p default martingales. The driver of the BSDE with multiple default jumps can take a generalized form involving an optional finite variation process. We first show existence and uniqueness. We then establish comparison and strict comparison results for these BSDEs, under a suitable assumption on the driver. In the case of a linear driver, we derive an explicit formula for the first component of the BSDE using an adjoint exponential semimartingale. The representation depends on whether the finite variation process is predictable or only optional. We apply our results to the problem of pricing and hedging a European option in a linear complete market with two defaultable assets and in a non-linear complete market with p defaultable assets. Two examples of the latter market model are provided: an example where the seller of the option is a large investor influencing the probability of default of a single asset and an example where the large seller's strategy affects the default probabilities of all p assets.

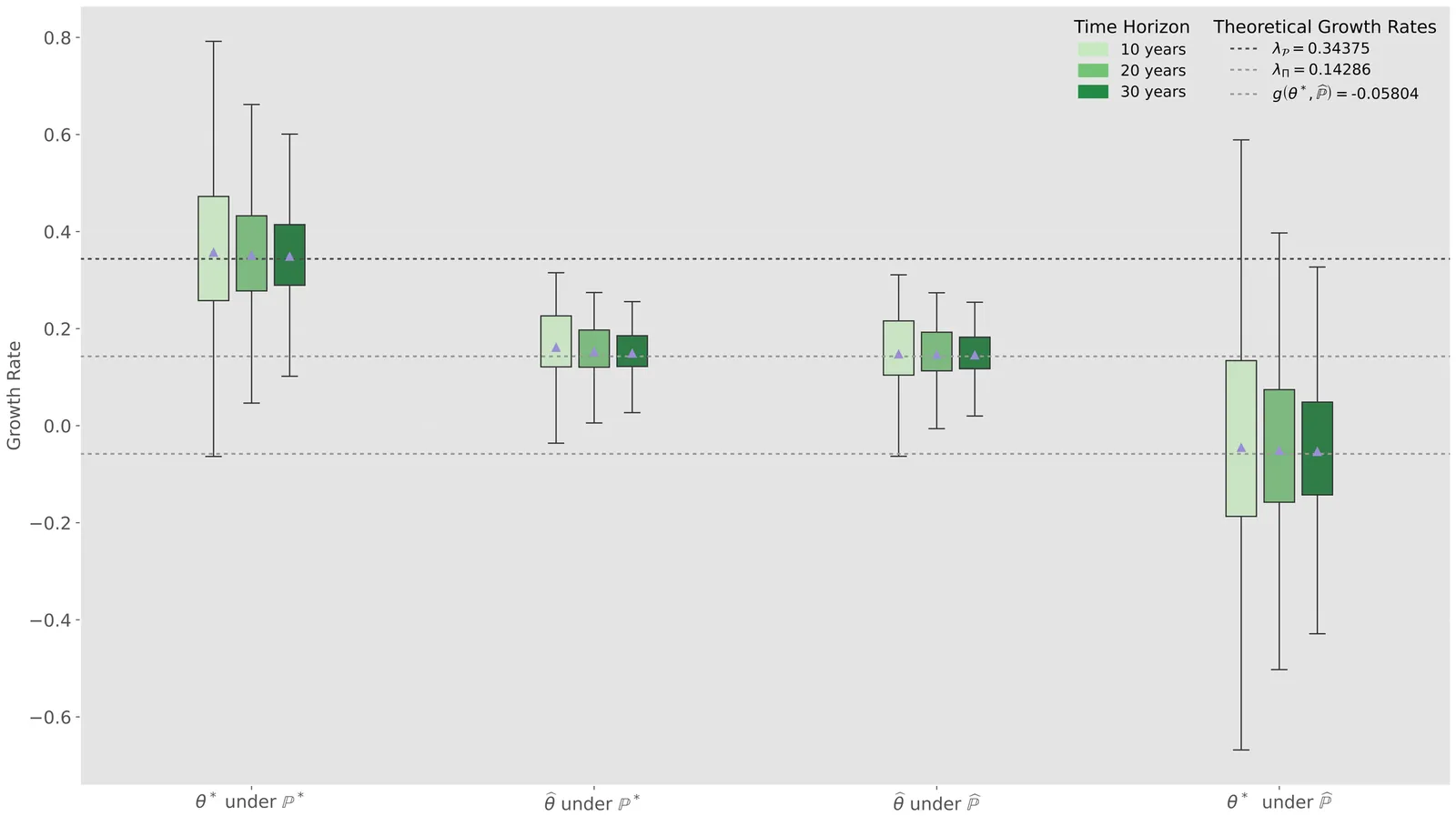

Drifts of asset returns are notoriously difficult to model accurately and, yet, trading strategies obtained from portfolio optimization are very sensitive to them. To mitigate this well-known phenomenon we study robust growth-optimization in a high-dimensional incomplete market under drift uncertainty of the asset price process $X$, under an additional ergodicity assumption, which constrains but does not fully specify the drift in general. The class of admissible models allows $X$ to depend on a multivariate stochastic factor $Y$ and fixes (a) their joint volatility structure, (b) their long-term joint ergodic density and (c) the dynamics of the stochastic factor process $Y$. A principal motivation of this framework comes from pairs trading, where $X$ is the spread process and models with the above characteristics are commonplace. Our main results determine the robust optimal growth rate, construct a worst-case admissible model and characterize the robust growth-optimal strategy via a solution to a certain partial differential equation (PDE). We demonstrate that utilizing the stochastic factor leads to improvement in robust growth complementing the conclusions of the previous study by Itkin et. al. (arXiv:2211.15628 [q-fin.MF], forthcoming in $\textit{Finance and Stochastics}$), which additionally robustified the dynamics of the stochastic factor leading to $Y$-independent optimal strategies. Our analysis leads to new financial insights, quantifying the improvement in growth the investor can achieve by optimally incorporating stochastic factors into their trading decisions. We illustrate our theoretical results on several numerical examples including an application to pairs trading.

The Lambda Value-at-Risk (Lambda$-VaR) is a generalization of the Value-at-Risk (VaR), which has been actively studied in quantitative finance. Over the past two decades, the Expected Shortfall (ES) has become one of the most important risk measures alongside VaR because of its various desirable properties in the practice of optimization, risk management, and financial regulation. Analogously to the intimate relation between ES and VaR, we introduce the Lambda Expected Shortfall (Lambda-ES), as a generalization of ES and a counterpart to Lambda-VaR. Our definition of Lambda-ES has an explicit formula and many convenient properties, and we show that it is the smallest quasi-convex and law-invariant risk measure dominating Lambda-VaR under mild assumptions. We examine further properties of Lambda-ES, its dual representation, and related optimization problems.

In the present paper, we study the near-maturity ($t\rightarrow T^{-}$) convergence rate of the optimal early-exercise price $b(t)$ of an American put under an exponential Lévy model with a {\it nonzero} Brownian component. Two important settings, not previous covered in the literature, are considered. In the case that the optimal exercise price converges to the strike price ($b(T^{-})=K$), we contemplate models with negative jumps of unbounded variation (i.e., processes that exhibit high activity of negative jumps or sudden falls in asset prices). In the second case, when the optimal exercise price tend to a value lower than $K$, we consider infinite activity jumps (though still of bounded variations), extending existing results for models with finite jump activity (finitely many jumps in any finite interval). In both cases, we show that $b(T^{-})-b(t)$ is of order $\sqrt{T-t}$ with explicit constants proportionality. Furthermore, we also derive the second-order near-maturity expansion of the American put price around the critical price along a certain parabolic branch.

We give a new formulation of the relative arbitrage problem from stochastic portfolio theory that asks for a time horizon beyond which arbitrage relative to the market exists in all ``sufficiently volatile'' markets. In our formulation, ``sufficiently volatile'' is interpreted as a lower bound on an ordered eigenvalue of the instantaneous covariation matrix, a quantity that has been studied extensively in the empirical finance literature. Upon framing the problem in the language of stochastic optimal control, we characterize the time horizon in question through the unique upper semicontinuous viscosity solution of a fully nonlinear elliptic partial differential equation (PDE). In a special case, this PDE amounts to the arrival time formulation of the Ambrosio-Soner co-dimension mean curvature flow. Beyond the setting of stochastic portfolio theory, the stochastic optimal control problem is analyzed for arbitrary compact, possibly non-convex, domains, thanks to a boundedness assumption on the instantaneous covariation matrix.

The estimation of the Risk Neutral Density (RND) implicit in option prices is challenging, especially in illiquid markets. We introduce the Deep Log-Sum-Exp Neural Network, an architecture that leverages Deep and Transfer learning to address RND estimation in the presence of irregular and illiquid strikes. We prove key statistical properties of the model and the consistency of the estimator. We illustrate the benefits of transfer learning to improve the estimation of the RND in severe illiquidity conditions through Monte Carlo simulations, and we test it empirically on SPX data, comparing it with popular estimation methods. Overall, our framework shows recovery of the RND in conditions of extreme illiquidity with as few as three option quotes.

We study the construction of arbitrage-free option price surfaces from noisy bid-ask quotes across strike and maturity. Our starting point is a Chebyshev representation of the call price surface on a warped log-moneyness/maturity rectangle, together with linear sampling and no-arbitrage operators acting on a collocation grid. Static no-arbitrage requirements are enforced as linear inequalities, while the surface is fitted directly to prices via a coverage-seeking quadratic objective that trades off squared band misfit against spectral and transport-inspired regularisation of the Chebyshev coefficients. This yields a strictly convex quadratic program in the modal coefficients, solvable at practical scales with off-the-shelf solvers (OSQP). On top of the global backbone, we introduce a local post-fit layer based on a discrete fog of risk-neutral densities on a three-dimensional lattice (m,t,u) and an associated Hamiltonian-type energy. On each patch of the (m,t) plane, the fog variables are coupled to a nodal price field obtained from the baseline surface, yielding a joint convex optimisation problem that reweights noisy quotes and applies noise-aware local corrections while preserving global static no-arbitrage and locality. The method is designed such that for equity options panels, the combined procedure achieves high inside-spread coverage in stable regimes (in calm years, 98-99% of quotes are priced inside the bid-ask intervals) and low rates of static no-arbitrage violations (below 1%). In stressed periods, the fog layer provides a mechanism for controlled leakage outside the band: when local quotes are mutually inconsistent or unusually noisy, the optimiser allocates fog mass outside the bid-ask tube and justifies small out-of-band deviations of the post-fit surface, while preserving a globally arbitrage-free and well-regularised description of the option surface.

We investigate the static portfolio selection problem of S-shaped and non-concave utility maximization under first-order and second-order stochastic dominance (SD) constraints. In many S-shaped utility optimization problems, one should require a liquidation boundary to guarantee the existence of a finite concave envelope function. A first-order SD (FSD) constraint can replace this requirement and provide an alternative for risk management. We explicitly solve the optimal solution under a general S-shaped utility function with a first-order stochastic dominance constraint. However, the second-order SD (SSD) constrained problem under non-concave utilities is difficult to solve analytically due to the invalidity of Sion's maxmin theorem. For this sake, we propose a numerical algorithm to obtain a plausible and sub-optimal solution for general non-concave utilities. The key idea is to detect the poor performance region with respect to the SSD constraints, characterize its structure and modify the distribution on that region to obtain (sub-)optimality. A key financial insight is that the decision maker should follow the SD constraint on the poor performance scenario while conducting the unconstrained optimal strategy otherwise. We provide numerical experiments to show that our algorithm effectively finds a sub-optimal solution in many cases. Finally, we develop an algorithm-guided piecewise-neural-network framework to learn the solution of the SSD problem, which demonstrates accelerated convergence compared to standard neural network approaches.

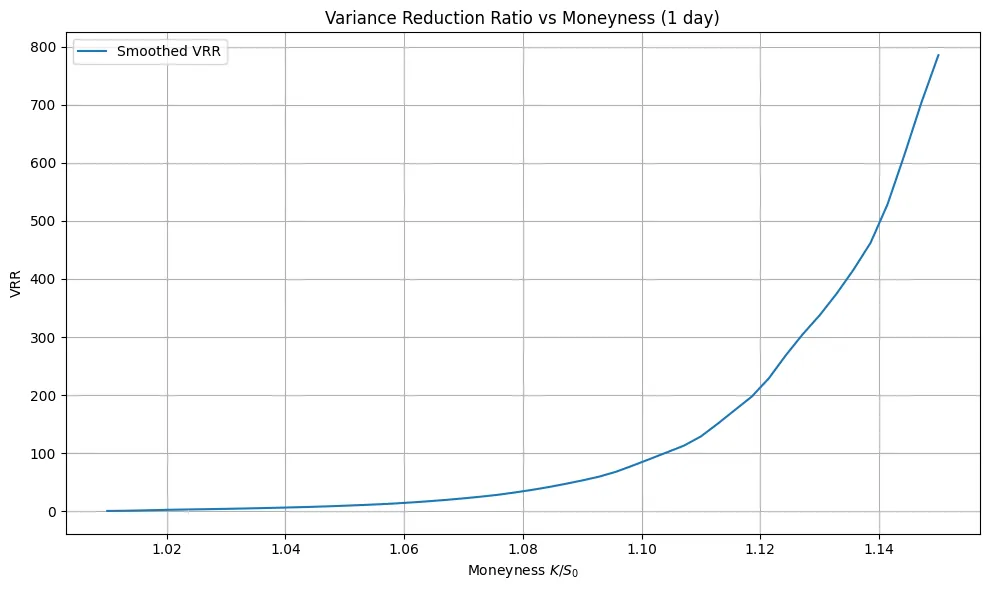

This paper investigates asymptotically optimal importance sampling (IS) schemes for pricing European call options under the Heston stochastic volatility model. We focus on two distinct rare-event regimes where standard Monte Carlo methods suffer from significant variance deterioration: the limit as maturity approaches zero and the limit as the strike price tends to infinity. Leveraging the large deviation principle (LDP), we design a state-dependent change of measure derived from the asymptotic behavior of the log-price cumulant generating functions. In the short-maturity regime, we rigorously prove that our proposed IS drift, inspired by the variational characterization of the rate function, achieves logarithmic efficiency (asymptotic optimality) by minimizing the decay rate of the second moment of the estimator. In the deep OTM regime, we introduce a novel slow mean-reversion scaling for the variance process, where the mean-reversion speed scales as the inverse square of the small-noise parameter (defined as the reciprocal of the log-moneyness). We establish that under this specific scaling, the variance process contributes non-trivially to the large deviation rate function, requiring a specialized Riccati analysis to verify optimality. Numerical experiments demonstrate that the proposed method yields substantial variance reduction--characterized by factors exceeding several orders of magnitude--compared to standard estimators in both asymptotic regimes.

We develop an arbitrage-free deep learning framework for yield curve and bond price forecasting based on the Heath-Jarrow-Morton (HJM) term-structure model and a dynamic Nelson-Siegel parameterization of forward rates. Our approach embeds a no-arbitrage drift restriction into a neural state-space architecture by combining Kalman, extended Kalman, and particle filters with recurrent neural networks (LSTM/CLSTM), and introduces an explicit arbitrage error regularization (AER) term during training. The model is applied to U.S. Treasury and corporate bond data, and its performance is evaluated for both yield-space and price-space predictions at 1-day and 5-day horizons. Empirically, arbitrage regularization leads to its strongest improvements at short maturities, particularly in 5-day-ahead forecasts, increasing market-consistency as measured by bid-ask hit rates and reducing dollar-denominated prediction errors.

Calibration of option pricing models is routinely repeated as markets evolve, yet modern systems lack an operator for removing data from a calibrated model without full retraining. When quotes become stale, corrupted, or subject to deletion requirements, existing calibration pipelines must rebuild the entire nonlinear least-squares problem, even if only a small subset of data must be excluded. In this work, we introduce a principled framework for selective forgetting (machine unlearning) in parametric option calibration. We provide stability guarantees, perturbation bounds, and show that the proposed operators satisfy local exactness under standard regularity assumptions.

In this work, we extend deep learning-based numerical methods to fully coupled forward-backward stochastic differential equations (FBSDEs) within a non-Markovian framework. Error estimates and convergence are provided. In contrast to the existing literature, our approach not only analyzes the non-Markovian framework but also addresses fully coupled settings, in which both the drift and diffusion coefficients of the forward process may be random and depend on the backward components $Y$ and $Z$. Furthermore, we illustrate the practical applicability of our framework by addressing utility maximization problems under rough volatility, which are solved numerically with the proposed deep learning-based methods.

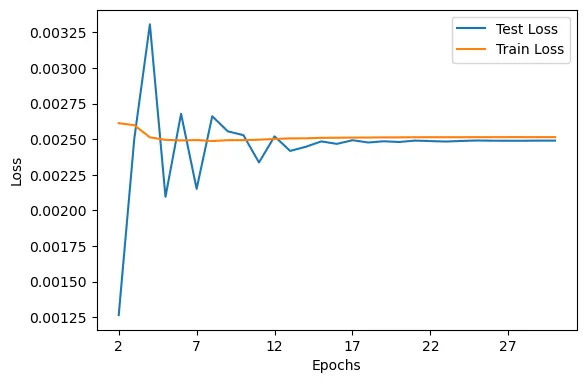

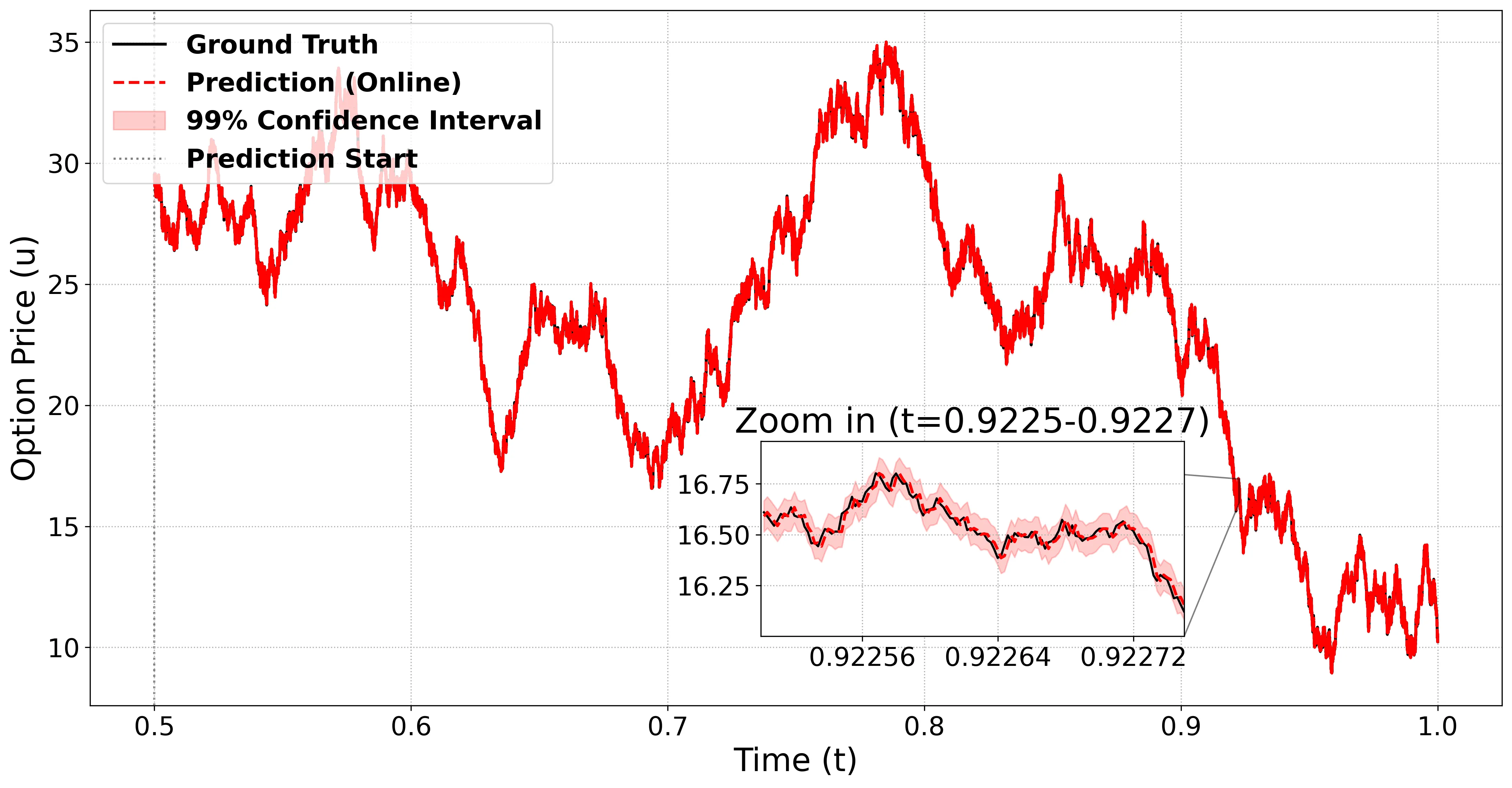

In this paper, we propose a novel data-driven framework for discovering probabilistic laws underlying the Feynman-Kac formula. Specifically, we introduce the first stochastic SINDy method formulated under the risk-neutral probability measure to recover the backward stochastic differential equation (BSDE) from a single pair of stock and option trajectories. Unlike existing approaches to identifying stochastic differential equations-which typically require ergodicity-our framework leverages the risk-neutral measure, thereby eliminating the ergodicity assumption and enabling BSDE recovery from limited financial time series data. Using this algorithm, we are able not only to make forward-looking predictions but also to generate new synthetic data paths consistent with the underlying probabilistic law.

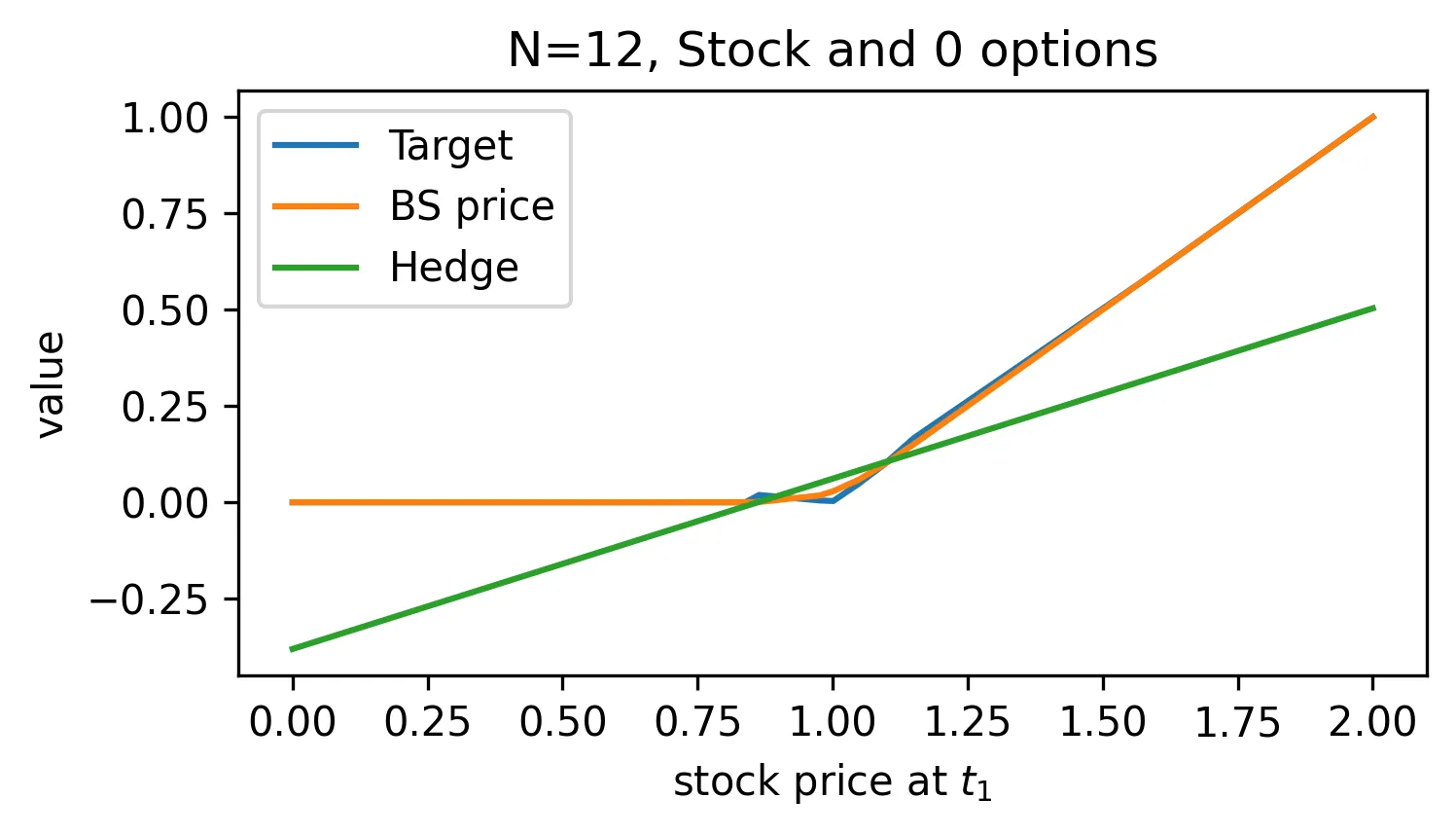

We consider an investor who wants to hedge a path-dependent option with maturity $T$ using a static hedging portfolio using cash, the underlying, and vanilla put/call options on the same underlying with maturity $ t_1$, where $0 < t_1 < T$. We propose a model-free approach to construct such a portfolio. The framework is inspired by the \textit{primal-dual} Martingale Optimal Transport (MOT) problem, which was pioneered by \cite{beiglbock2013model}. The optimization problem is to determine the portfolio composition that minimizes the expected worst-case hedging error at $t_1$ (that coincides with the maturity of the options that are used in the hedging portfolio). The worst-case scenario corresponds to the distribution that yields the worst possible hedging performance. This formulation leads to a \textit{min-max} problem. We provide a numerical scheme for solving this problem when a finite number of vanilla option prices are available. Numerical results on the hedging performance of this model-free approach when the option prices are generated using a \textit{Black-Scholes} and a \textit{Merton Jump diffusion} model are presented. We also provide theoretical bounds on the hedging error at $T$, the maturity of the target option.

We study a consumption-investment problem in a multi-asset market where the returns follow a generic rank-based model. Our main result derives an HJB equation with Neumann boundary conditions for the value function and proves a corresponding verification theorem. The control problem is nonstandard due to the discontinuous nature of the coefficients in rank-based models, requiring a bespoke approach of independent mathematical interest. The special case of first-order models, prescribing constant drift and diffusion coefficients for the ranked returns, admits explicit solutions when the investor is either (a) unconstrained, (b) abides by open market constraints or (c) is fully invested in the market. The explicit optimal strategies in all cases are related to the celebrated solution to Merton's problem, despite the intractability of constraint (b) in that setting.

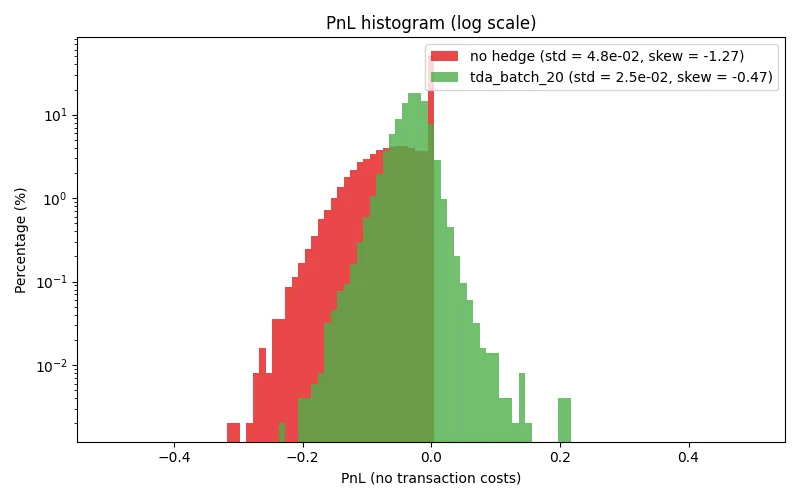

Deep hedging uses recurrent neural networks to hedge financial products that cannot be fully hedged in incomplete markets. Previous work in this area focuses on minimizing some measure of quadratic hedging error by calculating pathwise gradients, but doing so requires large batch sizes and can make training effective models in a reasonable amount of time challenging. We show that by adding certain topological features, we can reduce batch sizes substantially and make training these models more practically feasible without greatly compromising hedging performance.

In the context of time-subordinated Brownian motion models, Fourier theory and methodology are proposed to modelling the stochastic distribution of time increments. Gaussian Variance-Mean mixtures and time-subordinated models are reviewed with a key example being the Variance-Gamma process. A non-parametric characteristic function decomposition of subordinated Brownian motion is presented. The theory requires an extension of the real domain of certain characteristic functions to the complex plane, the validity of which is proven here. This allows one to characterise and study the stochastic time-change directly from the full process. An empirical decomposition of S\&P log-returns is provided to illustrate the methodology.

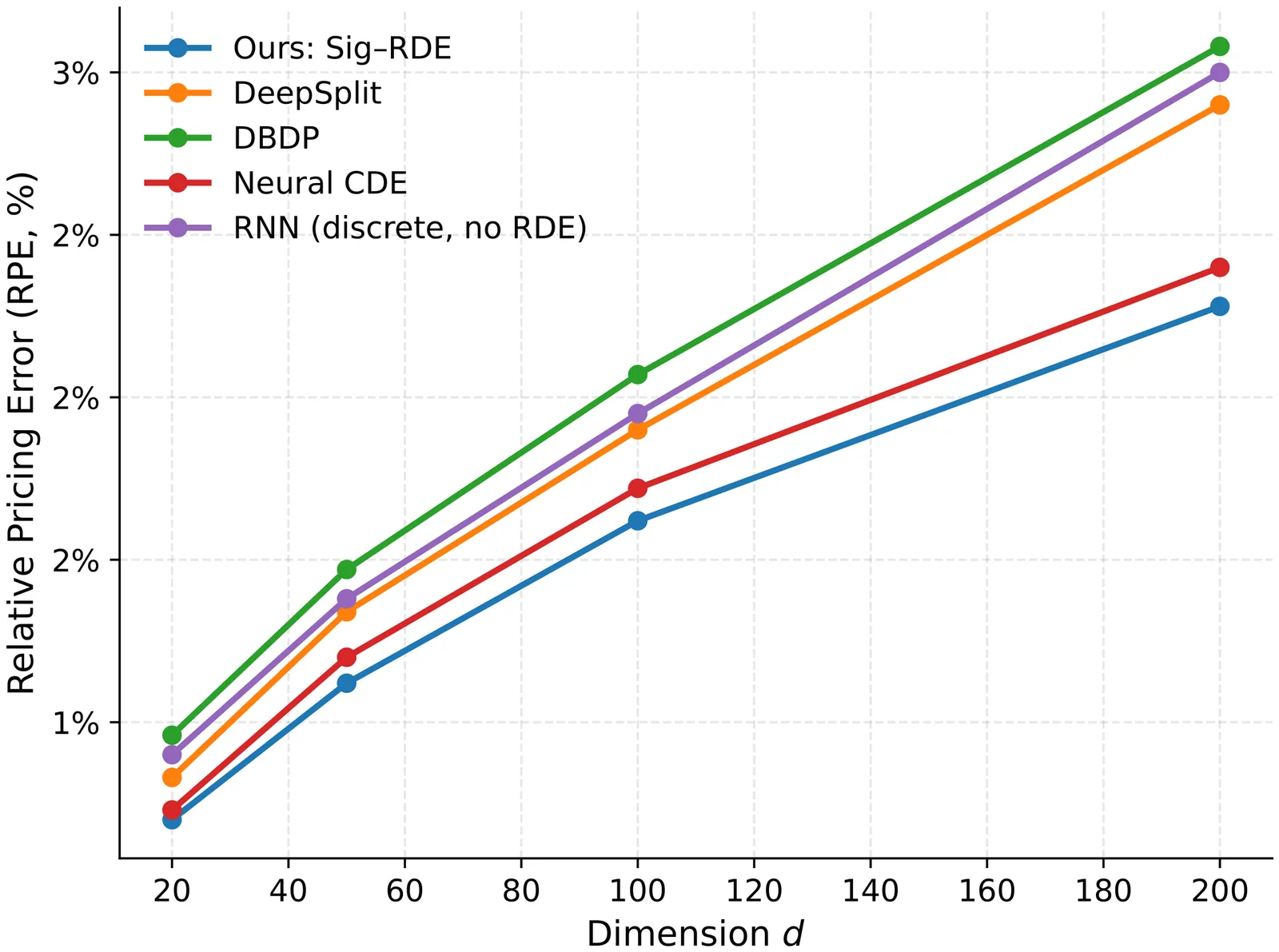

We tackle high-dimensional, path-dependent valuation and control and introduce a deep BSDE/2BSDE solver that couples truncated log-signatures with a neural rough differential equation (RDE) backbone. The architecture aligns stochastic analysis with sequence-to-path learning: a CVaR-tilted terminal objective targets left-tail risk, while an optional second-order (2BSDE) head supplies curvature estimates for risk-sensitive control. Under matched compute and parameter budgets, the method improves accuracy, tail fidelity, and training stability across Asian and barrier option pricing and portfolio control: at d=200 it achieves CVaR(0.99)=9.80% versus 12.00-13.10% for strong baselines, attains the lowest HJB residual (0.011), and yields the lowest RMSEs for Z and Gamma. Ablations over truncation depth, local windows, and tilt parameters confirm complementary gains from the sequence-to-path representation and the 2BSDE head. Taken together, the results highlight a bidirectional dialogue between stochastic analysis and modern deep learning: stochastic tools inform representations and objectives, while sequence-to-path models expand the class of solvable financial models at scale.