Trending in Mathematical Finance

Transfer Learning (Il)liquidity

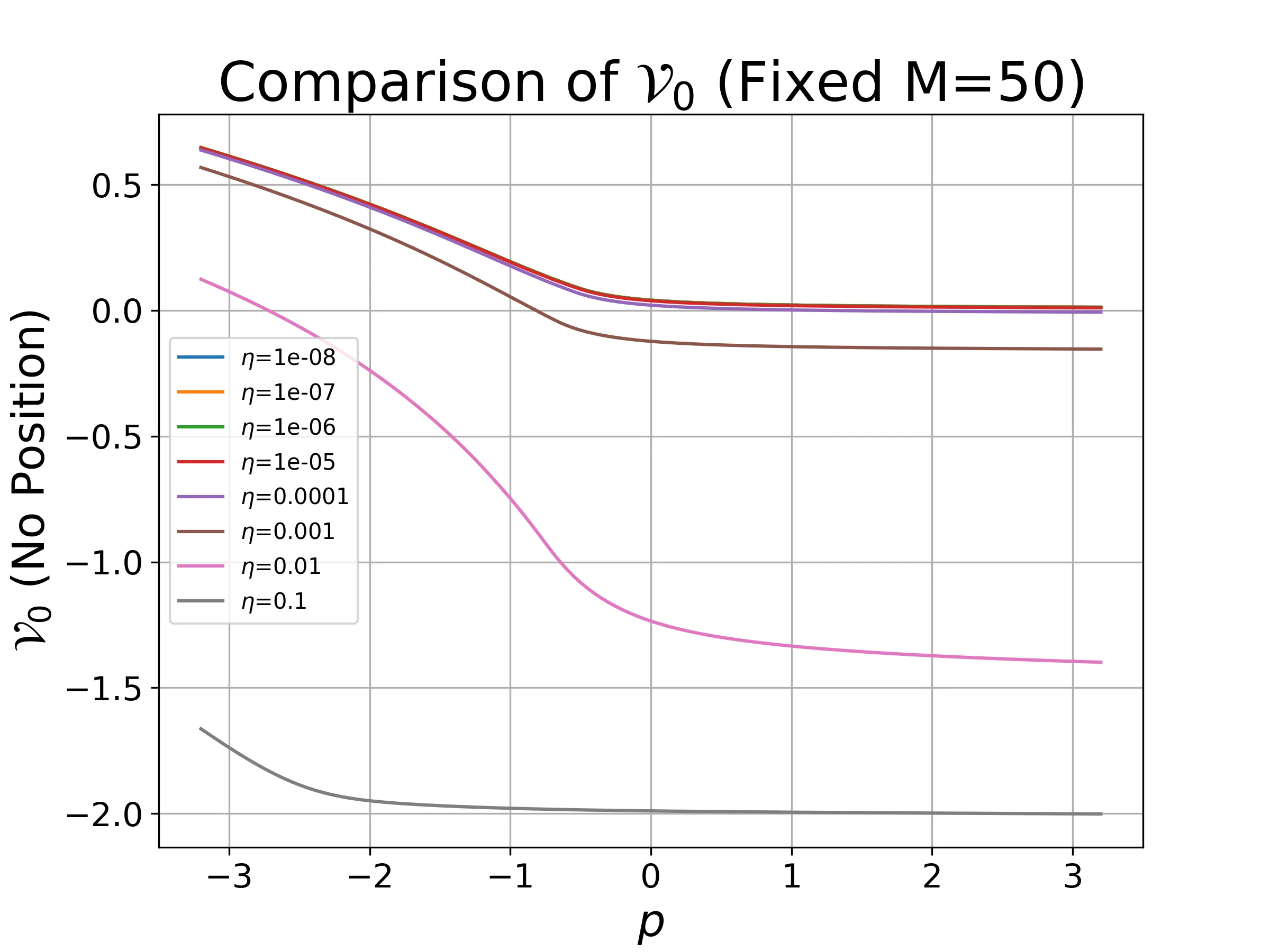

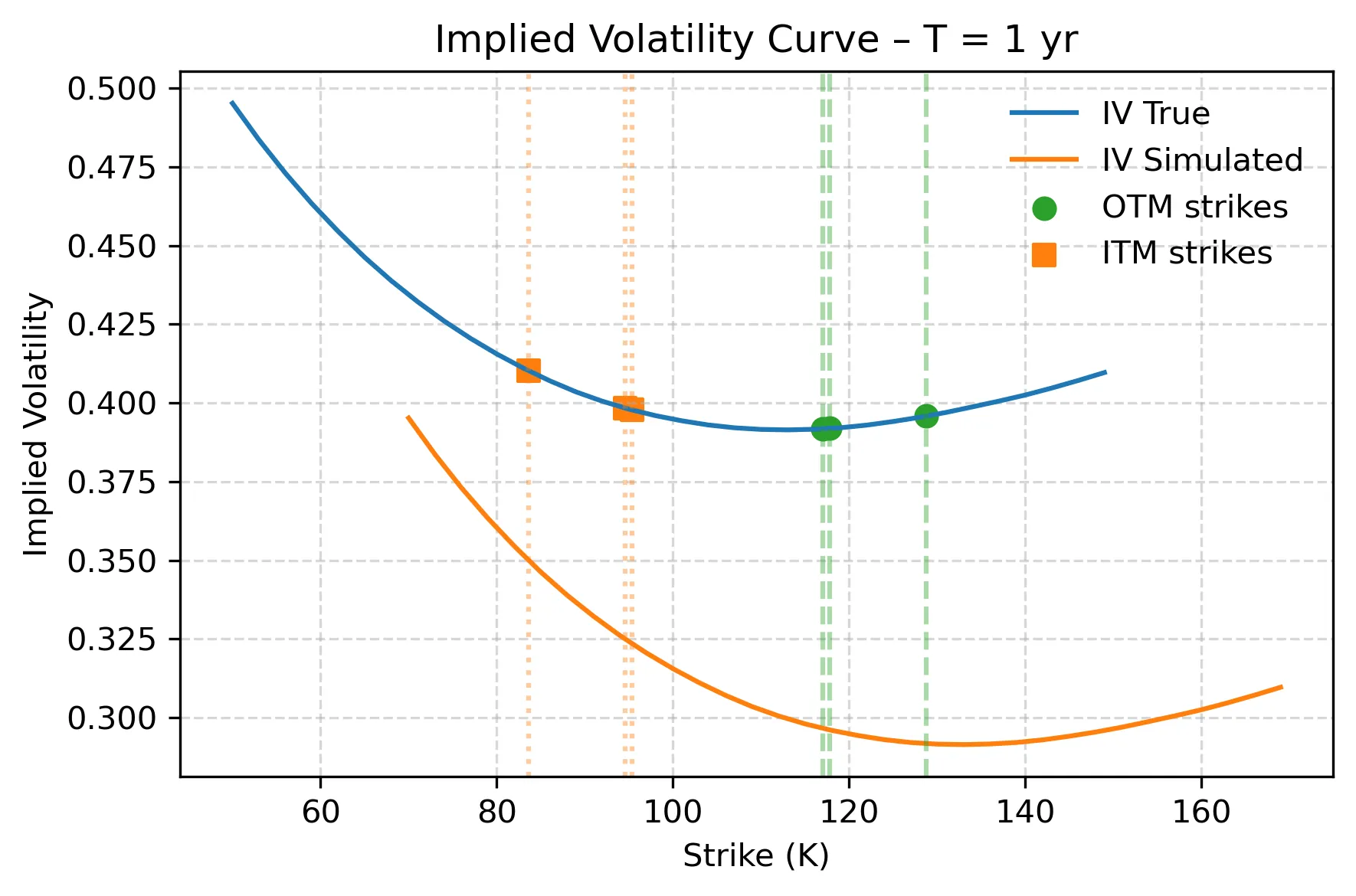

The estimation of the Risk Neutral Density (RND) implicit in option prices is challenging, especially in illiquid markets. We introduce the Deep Log-Sum-Exp Neural Network, an architecture that leverages Deep and Transfer learning to address RND estimation in the presence of irregular and illiquid strikes. We prove key statistical properties of the model and the consistency of the estimator. We illustrate the benefits of transfer learning to improve the estimation of the RND in severe illiquidity conditions through Monte Carlo simulations, and we test it empirically on SPX data, comparing it with popular estimation methods. Overall, our framework shows recovery of the RND in conditions of extreme illiquidity with as few as three option quotes.

2512.11731

Dec 2025Mathematical Finance

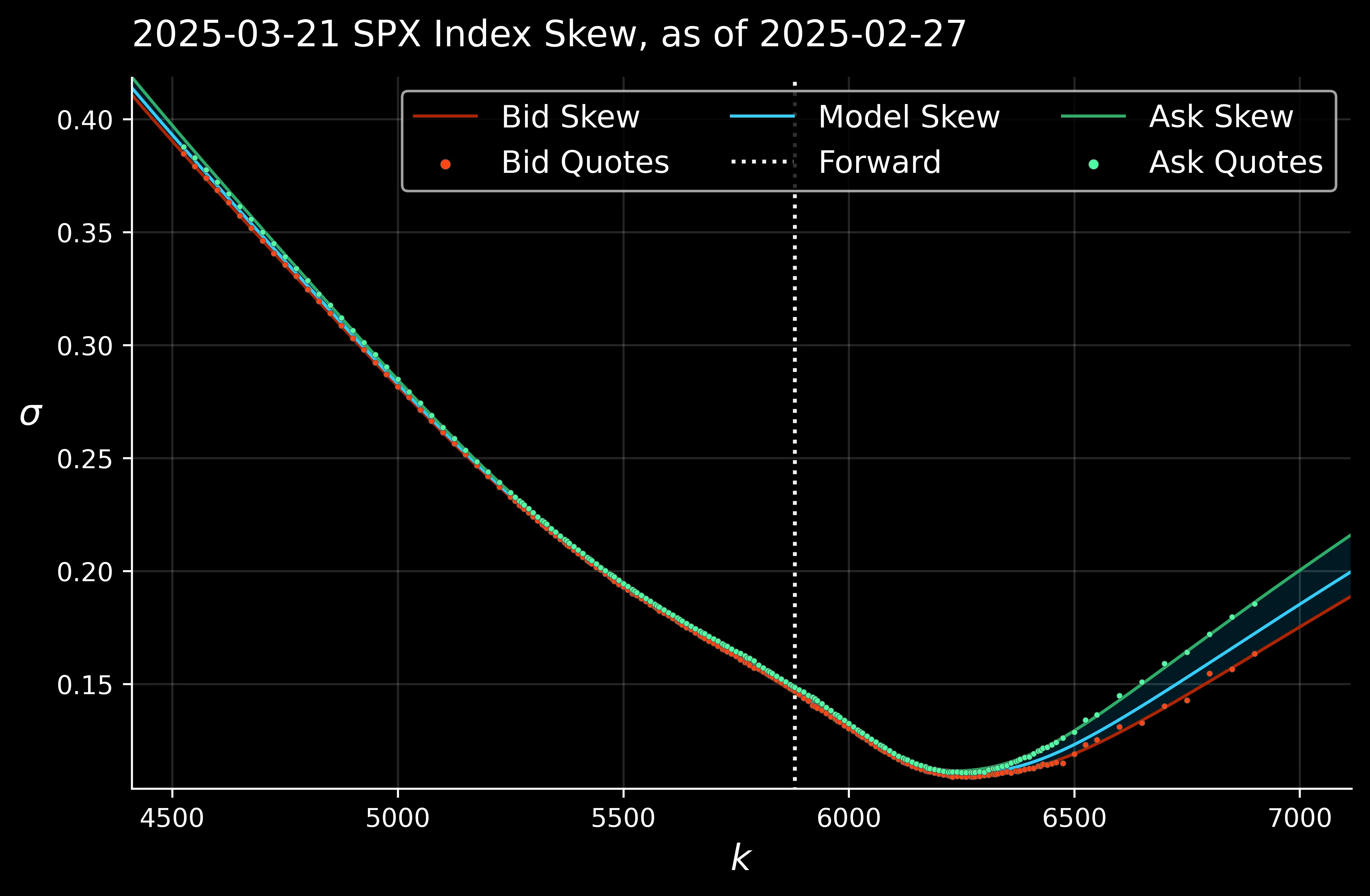

Arbitrage-Free Option Price Surfaces via Chebyshev Tensor Bases and a Hamiltonian Fog Post-Fit

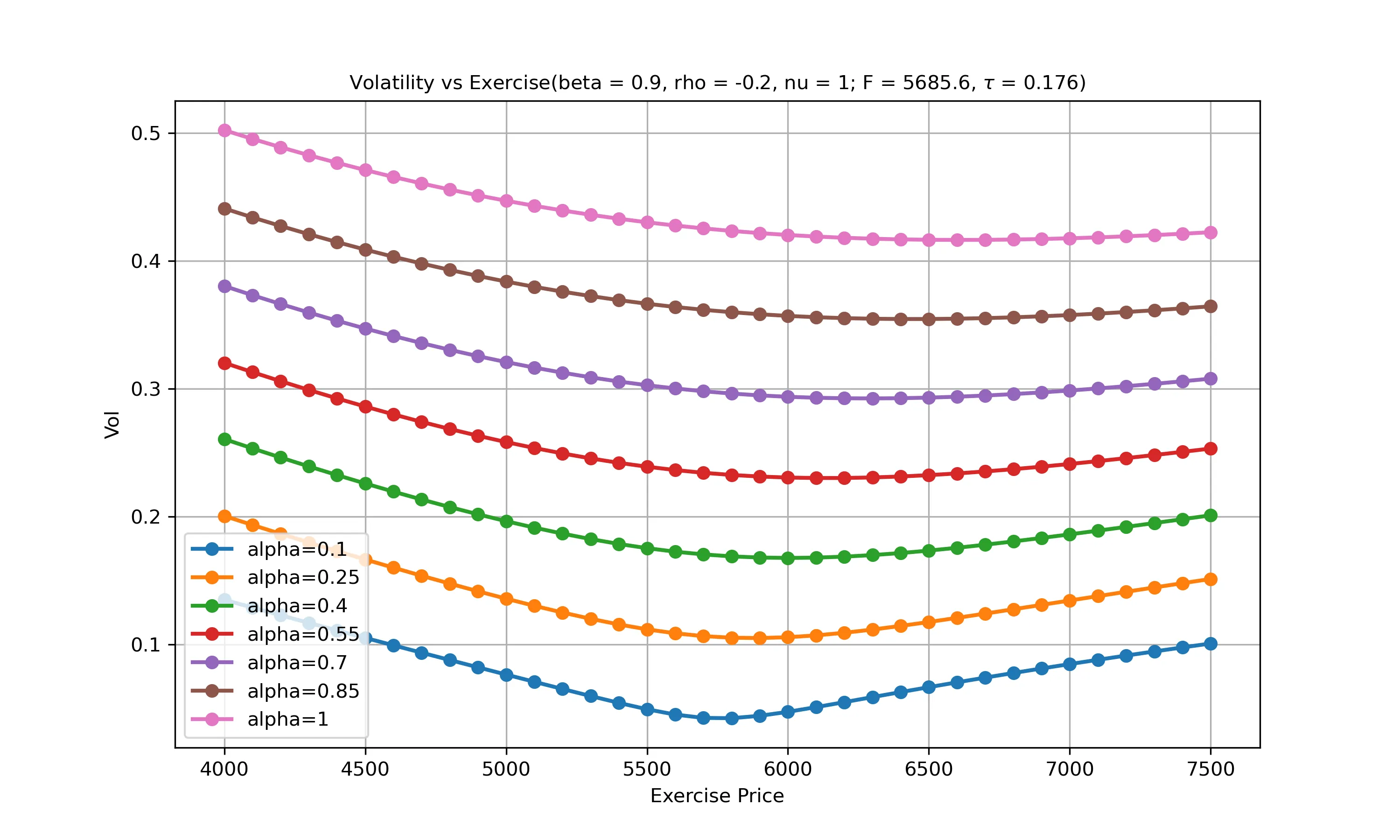

We study the construction of arbitrage-free option price surfaces from noisy bid-ask quotes across strike and maturity. Our starting point is a Chebyshev representation of the call price surface on a warped log-moneyness/maturity rectangle, together with linear sampling and no-arbitrage operators acting on a collocation grid. Static no-arbitrage requirements are enforced as linear inequalities, while the surface is fitted directly to prices via a coverage-seeking quadratic objective that trades off squared band misfit against spectral and transport-inspired regularisation of the Chebyshev coefficients. This yields a strictly convex quadratic program in the modal coefficients, solvable at practical scales with off-the-shelf solvers (OSQP). On top of the global backbone, we introduce a local post-fit layer based on a discrete fog of risk-neutral densities on a three-dimensional lattice (m,t,u) and an associated Hamiltonian-type energy. On each patch of the (m,t) plane, the fog variables are coupled to a nodal price field obtained from the baseline surface, yielding a joint convex optimisation problem that reweights noisy quotes and applies noise-aware local corrections while preserving global static no-arbitrage and locality. The method is designed such that for equity options panels, the combined procedure achieves high inside-spread coverage in stable regimes (in calm years, 98-99% of quotes are priced inside the bid-ask intervals) and low rates of static no-arbitrage violations (below 1%). In stressed periods, the fog layer provides a mechanism for controlled leakage outside the band: when local quotes are mutually inconsistent or unusually noisy, the optimiser allocates fog mass outside the bid-ask tube and justifies small out-of-band deviations of the post-fit surface, while preserving a globally arbitrage-free and well-regularised description of the option surface.

2512.01967

Dec 2025Mathematical Finance