Statistical Finance

arXiv:q-fin.ST

Statistical, econometric and econophysics analysis of financial markets.

Looking for a broader view? This category is part of:

Statistical, econometric and econophysics analysis of financial markets.

Looking for a broader view? This category is part of:

Synthetic financial data offers a practical way to address the privacy and accessibility challenges that limit research in quantitative finance. This paper examines the use of generative models, in particular TimeGAN and Variational Autoencoders (VAEs), for creating synthetic return series that support portfolio construction, trading analysis, and risk modeling. Using historical daily returns from the S and P 500 as a benchmark, we generate synthetic datasets under comparable market conditions and evaluate them using statistical similarity metrics, temporal structure tests, and downstream financial tasks. The study shows that TimeGAN produces synthetic data with distributional shapes, volatility patterns, and autocorrelation behaviour that are close to those observed in real returns. When applied to mean-variance portfolio optimization, the resulting synthetic datasets lead to portfolio weights, Sharpe ratios, and risk levels that remain close to those obtained from real data. The VAE provides more stable training but tends to smooth extreme market movements, which affects risk estimation. Finally, the analysis supports the use of synthetic datasets as substitutes for real financial data in portfolio analysis and risk simulation, particularly when models are able to capture temporal dynamics. Synthetic data therefore provides a privacy-preserving, cost-effective, and reproducible tool for financial experimentation and model development.

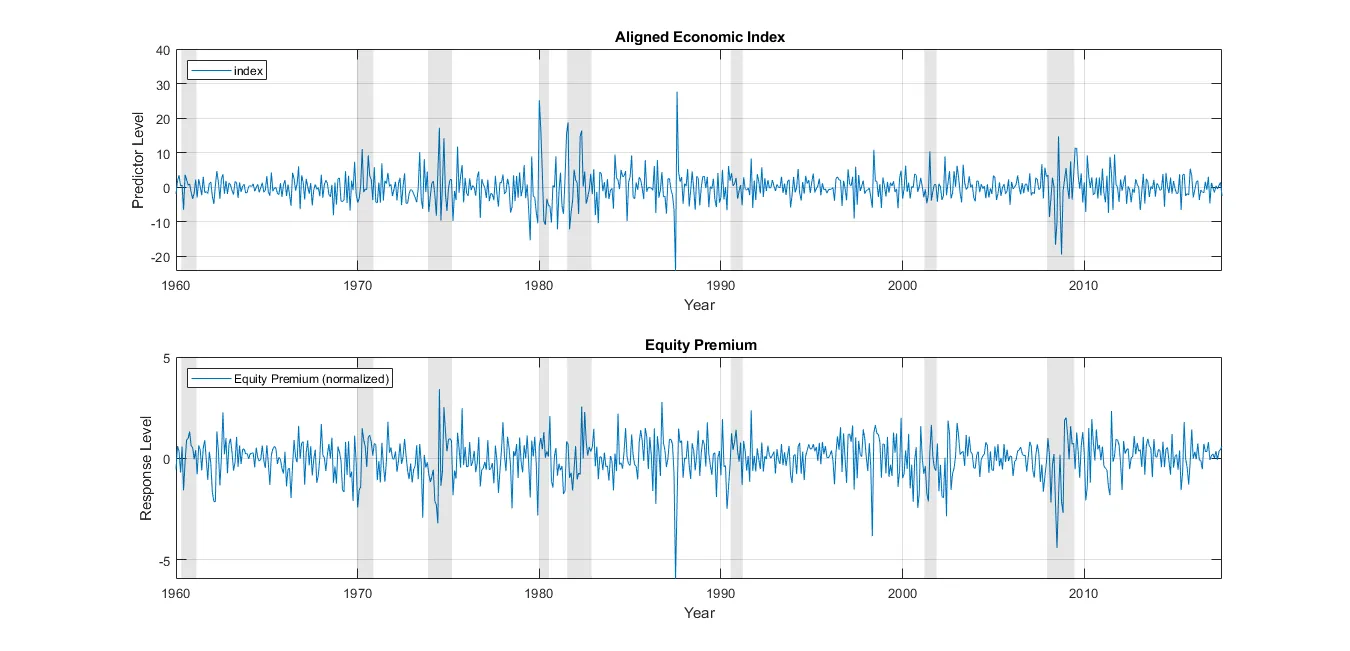

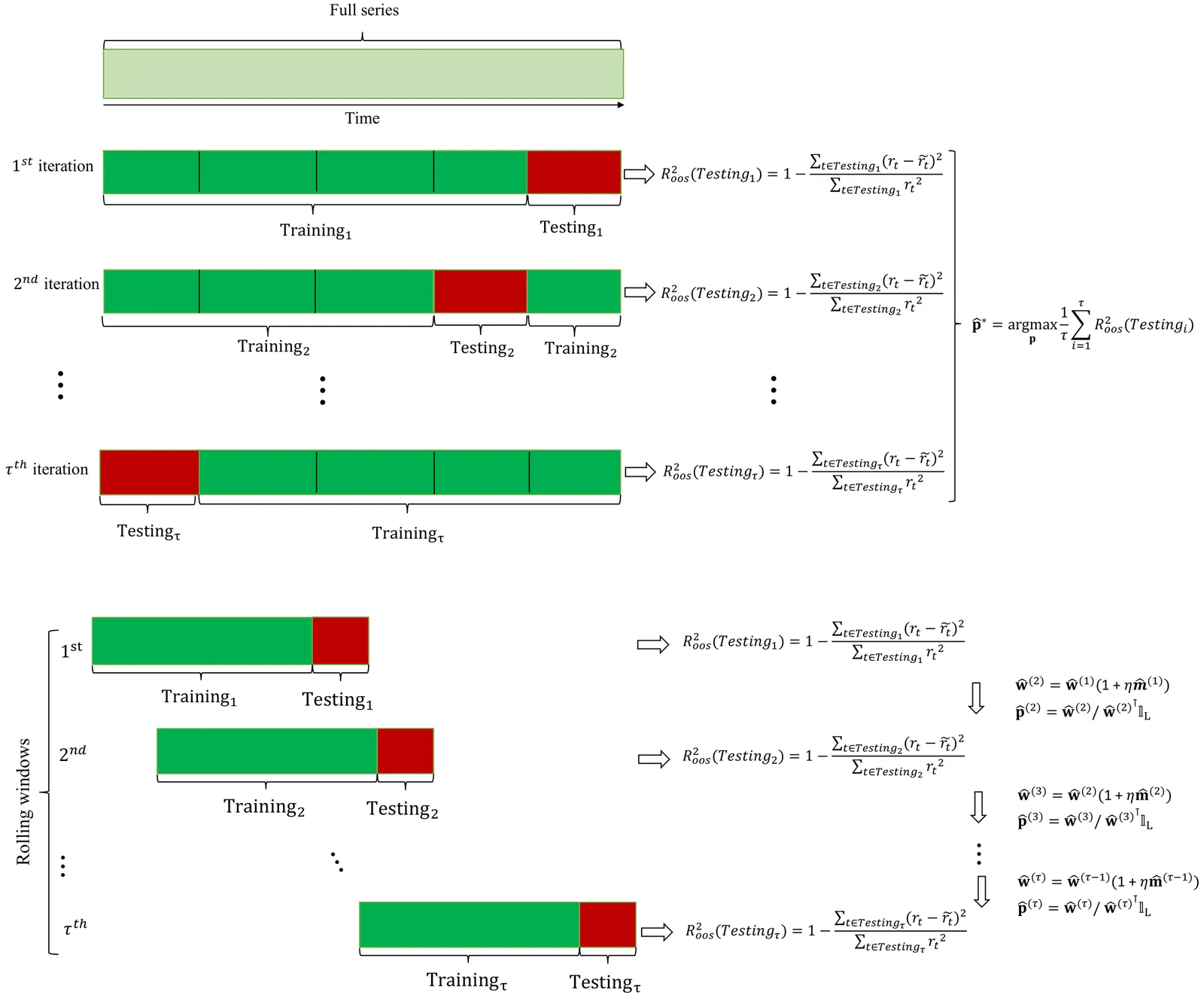

A growing empirical literature suggests that equity-premium predictability is state dependent, with much of the forecasting power concentrated around recessionary periods \parencite{Henkel2011,DanglHalling2012,Devpura2018}. I study U.S. stock return predictability across economic regimes and document strong evidence of time-varying expected returns across both expansionary and contractionary states. I contribute in two ways. First, I introduce a state-switching predictive regression in which the market state is defined in real time using the slope of the yield curve. Relative to the standard one-state predictive regression, the state-switching specification increases both in-sample and out-of-sample performance for the set of popular predictors considered by \textcite{WelchGoyal2008}, improving the out-of-sample performance of most predictors in economically meaningful ways. Second, I propose a new aggregate predictor, the Aligned Economic Index, constructed via partial least squares (PLS). Under the state-switching model, the Aligned Economic Index exhibits statistically and economically significant predictive power in sample and out of sample, and it outperforms widely used benchmark predictors and alternative predictor-combination methods.

We use a $φ^{4}$ quantum field theory with inhomogeneous couplings and explicit symmetry-breaking to model an ensemble of financial time series from the S$\&$P 500 index. The continuum nature of the $φ^4$ theory avoids the inaccuracies that occur in Ising-based models which require a discretization of the time series. We demonstrate this using the example of the 2008 global financial crisis. The $φ^{4}$ quantum field theory is expressive enough to reproduce the higher-order statistics such as the market kurtosis, which can serve as an indicator of possible market shocks. Accurate reproduction of high kurtosis is absent in binarized models. Therefore Ising models, despite being widely employed in econophysics, are incapable of fully representing empirical financial data, a limitation not present in the generalization of the $φ^{4}$ scalar field theory. We then investigate the scaling properties of the $φ^{4}$ machine learning algorithm and extract exponents which govern the behavior of the learned couplings (or weights and biases in ML language) in relation to the number of stocks in the model. Finally, we use our model to forecast the price changes of the AAPL, MSFT, and NVDA stocks. We conclude by discussing how the $φ^{4}$ scalar field theory could be used to build investment strategies and the possible intuitions that the QFT operations of dimensional compactification and renormalization can provide for financial modelling.

We study how generative artificial intelligence (AI) transforms the work of financial analysts. Using the 2023 launch of FactSet's AI platform as a natural experiment, we find that adoption produces markedly richer and more comprehensive reports -- featuring 40% more distinct information sources, 34% broader topical coverage, and 25% greater use of advanced analytical methods -- while also improving timeliness. However, forecast errors rise by 59% as AI-assisted reports convey a more balanced mix of positive and negative information that is harder to synthesize, particularly for analysts facing heavier cognitive demands. Placebo tests using other data vendors confirm that these effects are unique to FactSet's AI integration. Overall, our findings reveal both the productivity gains and cognitive limits of generative AI in financial information production.

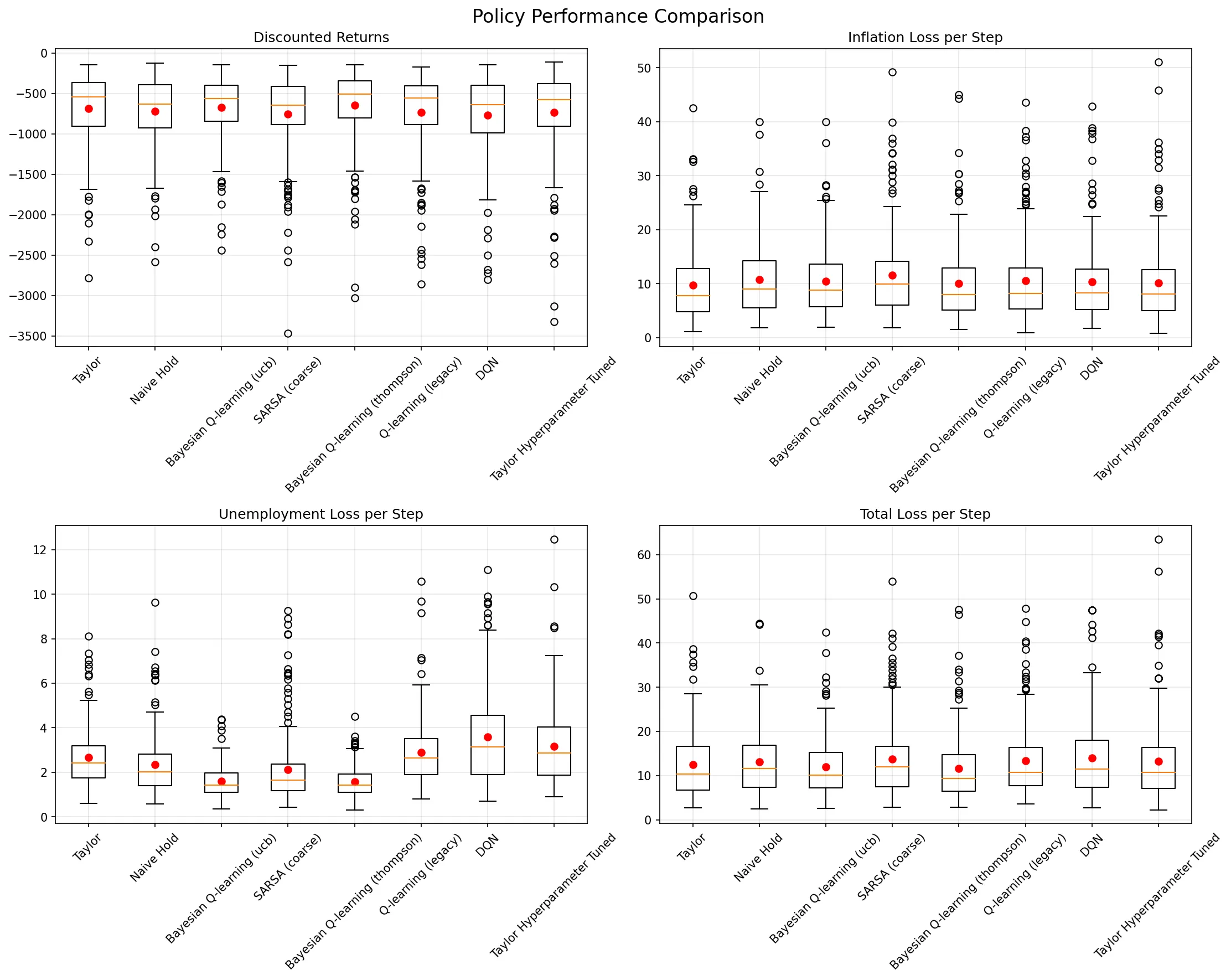

We study how a central bank should dynamically set short-term nominal interest rates to stabilize inflation and unemployment when macroeconomic relationships are uncertain and time-varying. We model monetary policy as a sequential decision-making problem where the central bank observes macroeconomic conditions quarterly and chooses interest rate adjustments. Using publically accessible historical Federal Reserve Economic Data (FRED), we construct a linear-Gaussian transition model and implement a discrete-action Markov Decision Process with a quadratic loss reward function. We chose to compare nine different reinforcement learning style approaches against Taylor Rule and naive baselines, including tabular Q-learning variants, SARSA, Actor-Critic, Deep Q-Networks, Bayesian Q-learning with uncertainty quantification, and POMDP formulations with partial observability. Surprisingly, standard tabular Q-learning achieved the best performance (-615.13 +- 309.58 mean return), outperforming both enhanced RL methods and traditional policy rules. Our results suggest that while sophisticated RL techniques show promise for monetary policy applications, simpler approaches may be more robust in this domain, highlighting important challenges in applying modern RL to macroeconomic policy.

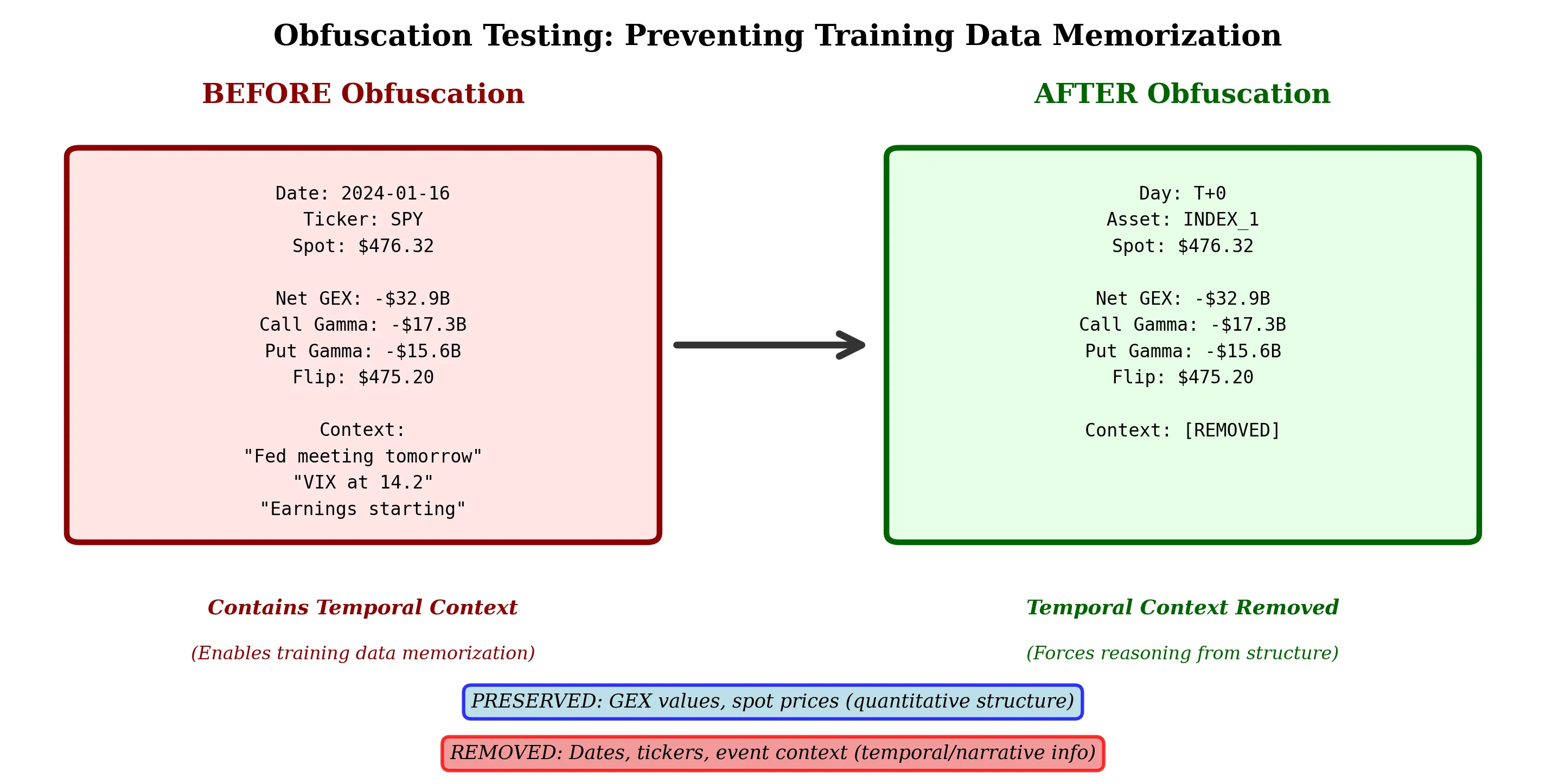

We introduce obfuscation testing, a novel methodology for validating whether large language models detect structural market patterns through causal reasoning rather than temporal association. Testing three dealer hedging constraint patterns (gamma positioning, stock pinning, 0DTE hedging) on 242 trading days (95.6% coverage) of S&P 500 options data, we find LLMs achieve 71.5% detection rate using unbiased prompts that provide only raw gamma exposure values without regime labels or temporal context. The WHO-WHOM-WHAT causal framework forces models to identify the economic actors (dealers), affected parties (directional traders), and structural mechanisms (forced hedging) underlying observed market dynamics. Critically, detection accuracy (91.2%) remains stable even as economic profitability varies quarterly, demonstrating that models identify structural constraints rather than profitable patterns. When prompted with regime labels, detection increases to 100%, but the 71.5% unbiased rate validates genuine pattern recognition. Our findings suggest LLMs possess emergent capabilities for detecting complex financial mechanisms through pure structural reasoning, with implications for systematic strategy development, risk management, and our understanding of how transformer architectures process financial market dynamics.

Correlations in complex systems are often obscured by nonstationarity, long-range memory, and heavy-tailed fluctuations, which limit the usefulness of traditional covariance-based analyses. To address these challenges, we construct scale and fluctuation-dependent correlation matrices using the multifractal detrended cross-correlation coefficient $ρ_r$ that selectively emphasizes fluctuations of different amplitudes. We examine the spectral properties of these detrended correlation matrices and compare them to the spectral properties of the matrices calculated in the same way from synthetic Gaussian and $q$Gaussian signals. Our results show that detrending, heavy tails, and the fluctuation-order parameter $r$ jointly produce spectra, which substantially depart from the random case even under absence of cross-correlations in time series. Applying this framework to one-minute returns of 140 major cryptocurrencies from 2021-2024 reveals robust collective modes, including a dominant market factor and several sectoral components whose strength depends on the analyzed scale and fluctuation order. After filtering out the market mode, the empirical eigenvalue bulk aligns closely with the limit of random detrended cross-correlations, enabling clear identification of structurally significant outliers. Overall, the study provides a refined spectral baseline for detrended cross-correlations and offers a promising tool for distinguishing genuine interdependencies from noise in complex, nonstationary, heavy-tailed systems.

This paper investigates an optimal integration of deep learning with financial models for robust asset price forecasting. Specifically, we developed a hybrid framework combining a Long Short-Term Memory (LSTM) network with the Merton-Lévy jump-diffusion model. To optimise this framework, we employed the Grey Wolf Optimizer (GWO) for the LSTM hyperparameter tuning, and we explored three calibration methods for the Merton-Levy model parameters: Artificial Neural Networks (ANNs), the Marine Predators Algorithm (MPA), and the PyTorch-based TorchSDE library. To evaluate the predictive performance of our hybrid model, we compared it against several benchmark models, including a standard LSTM and an LSTM combined with the Fractional Heston model. This evaluation used three real-world financial datasets: Brent oil prices, the STOXX 600 index, and the IT40 index. Performance was assessed using standard metrics, including Mean Squared Error (MSE), Mean Absolute Error(MAE), Mean Squared Percentage Error (MSPE), and the coefficient of determination (R2). Our experimental results demonstrate that the hybrid model, combining a GWO-optimized LSTM network with the Levy-Merton Jump-Diffusion model calibrated using an ANN, outperformed the base LSTM model and all other models developed in this study.

Forecasting cryptocurrency prices is hindered by extreme volatility and a methodological dilemma between information-scarce univariate models and noise-prone full-multivariate models. This paper investigates a partial-multivariate approach to balance this trade-off, hypothesizing that a strategic subset of features offers superior predictive power. We apply the Partial-Multivariate Transformer (PMformer) to forecast daily returns for BTCUSDT and ETHUSDT, benchmarking it against eleven classical and deep learning models. Our empirical results yield two primary contributions. First, we demonstrate that the partial-multivariate strategy achieves significant statistical accuracy, effectively balancing informative signals with noise. Second, we experiment and discuss an observable disconnect between this statistical performance and practical trading utility; lower prediction error did not consistently translate to higher financial returns in simulations. This finding challenges the reliance on traditional error metrics and highlights the need to develop evaluation criteria more aligned with real-world financial objectives.

We study a systematic approach to a popular Statistical Arbitrage technique: Pairs Trading. Instead of relying on two highly correlated assets, we replace the second asset with a replication of the first using risk factor representations. These factors are obtained through Principal Components Analysis (PCA), exchange traded funds (ETFs), and, as our main contribution, Long Short Term Memory networks (LSTMs). Residuals between the main asset and its replication are examined for mean reversion properties, and trading signals are generated for sufficiently fast mean reverting portfolios. Beyond introducing a deep learning based replication method, we adapt the framework of Avellaneda and Lee (2008) to the Polish market. Accordingly, components of WIG20, mWIG40, and selected sector indices replace the original S&P500 universe, and market parameters such as the risk free rate and transaction costs are updated to reflect local conditions. We outline the full strategy pipeline: risk factor construction, residual modeling via the Ornstein Uhlenbeck process, and signal generation. Each replication technique is described together with its practical implementation. Strategy performance is evaluated over two periods: 2017-2019 and the recessive year 2020. All methods yield profits in 2017-2019, with PCA achieving roughly 20 percent cumulative return and an annualized Sharpe ratio of up to 2.63. Despite multiple adaptations, our conclusions remain consistent with those of the original paper. During the COVID-19 recession, only the ETF based approach remains profitable (about 5 percent annual return), while PCA and LSTM methods underperform. LSTM results, although negative, are promising and indicate potential for future optimization.

We investigate a number of Artificial Neural Network architectures (well-known and more ``exotic'') in application to the long-term financial time-series forecasts of indexes on different global markets. The particular area of interest of this research is to examine the correlation of these indexes' behaviour in terms of Machine Learning algorithms cross-training. Would training an algorithm on an index from one global market produce similar or even better accuracy when such a model is applied for predicting another index from a different market? The demonstrated predominately positive answer to this question is another argument in favour of the long-debated Efficient Market Hypothesis of Eugene Fama.

Starting from the Pearson Correlation Matrix of stock returns and from the desire to obtain a reduced number of parameters relevant for the dynamics of a financial market, we propose to take the idea of a sectorial matrix, which would have a large number of parameters, to the reduced picture of a real symmetric $2 \times 2$ matrix, extreme case, that still conserves the desirable feature that the average correlation can be one of the parameters. This is achieved by averaging the correlation matrix over blocks created by choosing two subsets of stocks for rows and columns and averaging over each of the resulting blocks. Averaging over these blocks, we retain the average of the correlation matrix. We shall use a random selection for two equal block sizes as well as two specific, hopefully relevant, ones that do not produce equal block sizes. The results show that one of the non-random choices has somewhat different properties, whose meaning will have to be analyzed from an economy point of view.

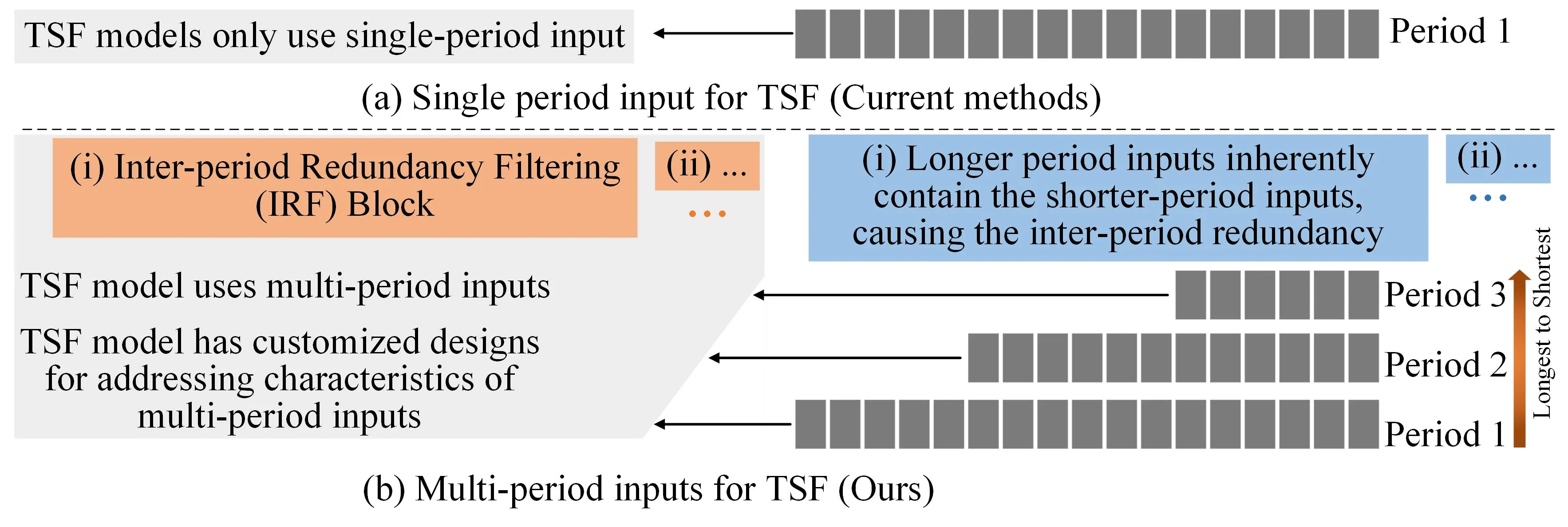

Time series forecasting is important in finance domain. Financial time series (TS) patterns are influenced by both short-term public opinions and medium-/long-term policy and market trends. Hence, processing multi-period inputs becomes crucial for accurate financial time series forecasting (TSF). However, current TSF models either use only single-period input, or lack customized designs for addressing multi-period characteristics. In this paper, we propose a Multi-period Learning Framework (MLF) to enhance financial TSF performance. MLF considers both TSF's accuracy and efficiency requirements. Specifically, we design three new modules to better integrate the multi-period inputs for improving accuracy: (i) Inter-period Redundancy Filtering (IRF), that removes the information redundancy between periods for accurate self-attention modeling, (ii) Learnable Weighted-average Integration (LWI), that effectively integrates multi-period forecasts, (iii) Multi-period self-Adaptive Patching (MAP), that mitigates the bias towards certain periods by setting the same number of patches across all periods. Furthermore, we propose a Patch Squeeze module to reduce the number of patches in self-attention modeling for maximized efficiency. MLF incorporates multiple inputs with varying lengths (periods) to achieve better accuracy and reduces the costs of selecting input lengths during training. The codes and datasets are available at https://github.com/Meteor-Stars/MLF.

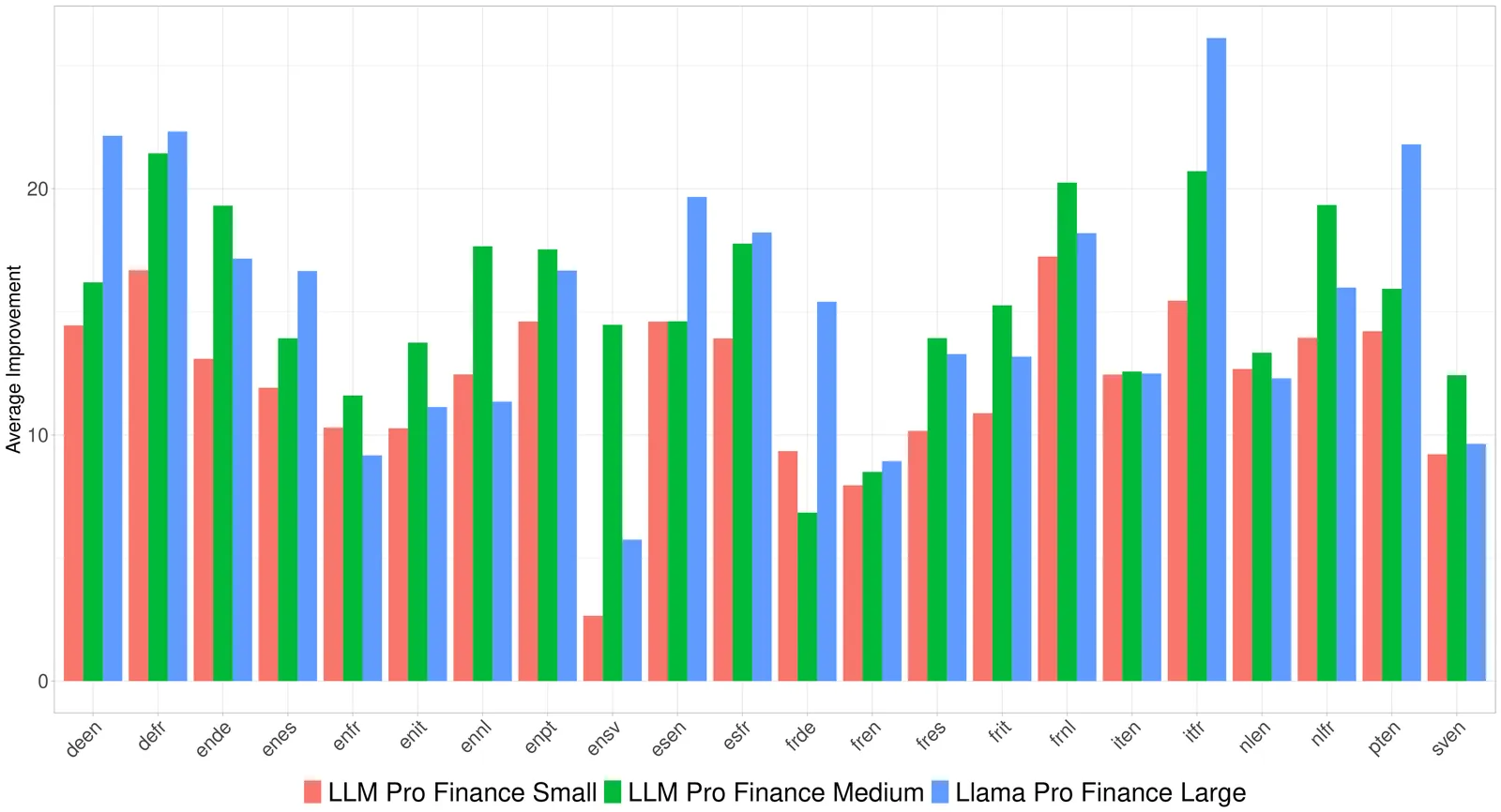

The financial industry's growing demand for advanced natural language processing (NLP) capabilities has highlighted the limitations of generalist large language models (LLMs) in handling domain-specific financial tasks. To address this gap, we introduce the LLM Pro Finance Suite, a collection of five instruction-tuned LLMs (ranging from 8B to 70B parameters) specifically designed for financial applications. Our approach focuses on enhancing generalist instruction-tuned models, leveraging their existing strengths in instruction following, reasoning, and toxicity control, while fine-tuning them on a curated, high-quality financial corpus comprising over 50% finance-related data in English, French, and German. We evaluate the LLM Pro Finance Suite on a comprehensive financial benchmark suite, demonstrating consistent improvement over state-of-the-art baselines in finance-oriented tasks and financial translation. Notably, our models maintain the strong general-domain capabilities of their base models, ensuring reliable performance across non-specialized tasks. This dual proficiency, enhanced financial expertise without compromise on general abilities, makes the LLM Pro Finance Suite an ideal drop-in replacement for existing LLMs in financial workflows, offering improved domain-specific performance while preserving overall versatility. We publicly release two 8B-parameters models to foster future research and development in financial NLP applications: https://huggingface.co/collections/DragonLLM/llm-open-finance.

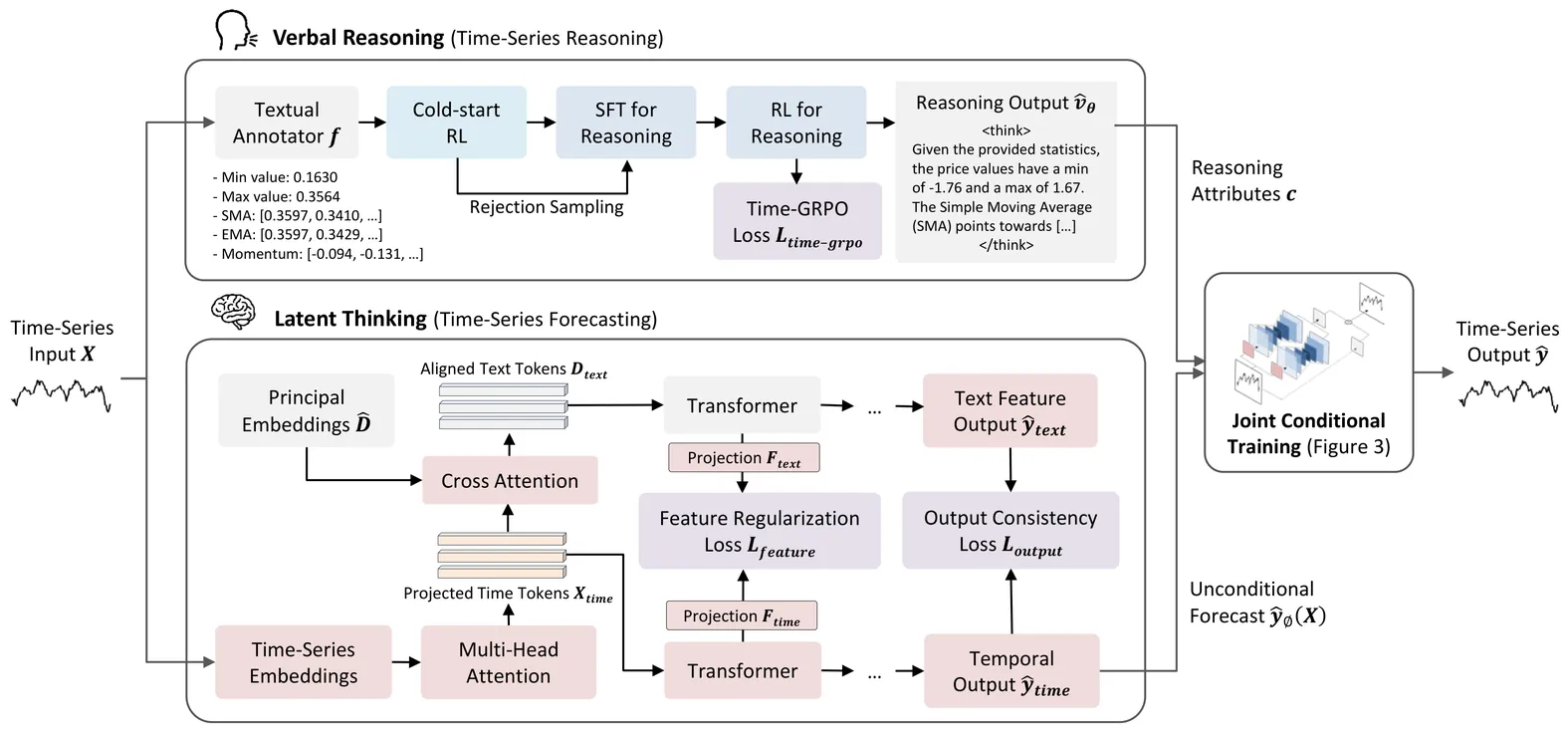

While Large Language Models have been used to produce interpretable stock forecasts, they mainly focus on analyzing textual reports but not historical price data, also known as Technical Analysis. This task is challenging as it switches between domains: the stock price inputs and outputs lie in the time-series domain, while the reasoning step should be in natural language. In this work, we introduce Verbal Technical Analysis (VTA), a novel framework that combine verbal and latent reasoning to produce stock time-series forecasts that are both accurate and interpretable. To reason over time-series, we convert stock price data into textual annotations and optimize the reasoning trace using an inverse Mean Squared Error (MSE) reward objective. To produce time-series outputs from textual reasoning, we condition the outputs of a time-series backbone model on the reasoning-based attributes. Experiments on stock datasets across U.S., Chinese, and European markets show that VTA achieves state-of-the-art forecasting accuracy, while the reasoning traces also perform well on evaluation by industry experts.

We study opportunistic optimal liquidation over fixed deadlines on BTC-USD limit-order books (LOB). We present RL-Exec, a PPO agent trained on historical replays augmented with endogenous transient impact (resilience), partial fills, maker/taker fees, and latency. The policy observes depth-20 LOB features plus microstructure indicators and acts under a sell-only inventory constraint to reach a residual target. Evaluation follows a strict time split (train: Jan-2020; test: Feb-2020) and a per-day protocol: for each test day we run ten independent start times and aggregate to a single daily score, avoiding pseudo-replication. We compare the agent to (i) TWAP and (ii) a VWAP-like baseline allocating using opposite-side order-book liquidity (top-20 levels), both executed on identical timestamps and costs. Statistical inference uses one-sided Wilcoxon signed-rank tests on daily RL-baseline differences with Benjamini-Hochberg FDR correction and bootstrap confidence intervals. On the Feb-2020 test set, RL-Exec significantly outperforms both baselines and the gap increases with the execution horizon (+2-3 bps at 30 min, +7-8 bps at 60 min, +23 bps at 120 min). Code: github.com/Giafferri/RL-Exec

Electricity price forecasting has become a critical tool for decision-making in energy markets, particularly as the increasing penetration of renewable energy introduces greater volatility and uncertainty. Historically, research in this field has been dominated by point forecasting methods, which provide single-value predictions but fail to quantify uncertainty. However, as power markets evolve due to renewable integration, smart grids, and regulatory changes, the need for probabilistic forecasting has become more pronounced, offering a more comprehensive approach to risk assessment and market participation. This paper presents a review of probabilistic forecasting methods, tracing their evolution from Bayesian and distribution based approaches, through quantile regression techniques, to recent developments in conformal prediction. Particular emphasis is placed on advancements in probabilistic forecasting, including validity-focused methods which address key limitations in uncertainty estimation. Additionally, this review extends beyond the Day-Ahead Market to include the Intra-Day and Balancing Markets, where forecasting challenges are intensified by higher temporal granularity and real-time operational constraints. We examine state of the art methodologies, key evaluation metrics, and ongoing challenges, such as forecast validity, model selection, and the absence of standardised benchmarks, providing researchers and practitioners with a comprehensive and timely resource for navigating the complexities of modern electricity markets.

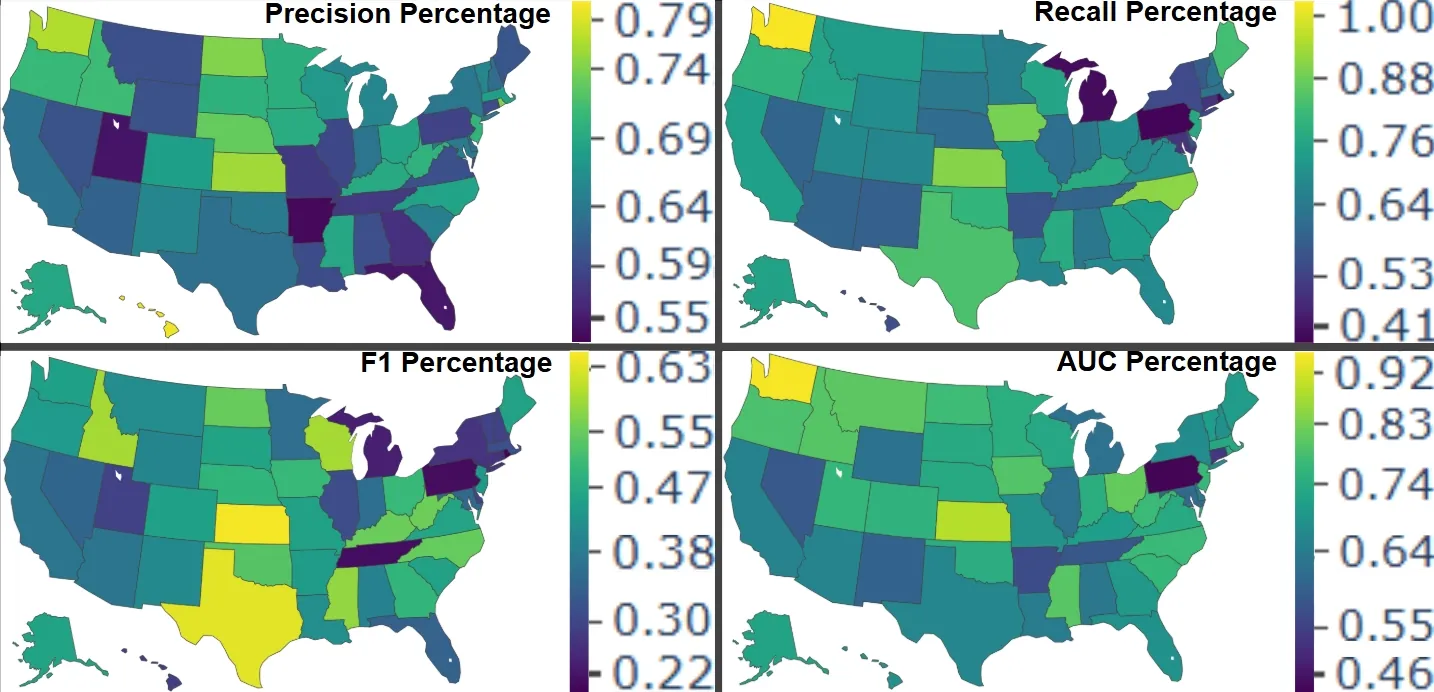

We present the first application of federated learning (FL) to the U.S. National Financial Capability Study, introducing an interpretable framework for predicting consumer financial distress across all 50 states and the District of Columbia without centralizing sensitive data. Our cross-silo FL setup treats each state as a distinct data silo, simulating real-world governance in nationwide financial systems. Unlike prior work, our approach integrates two complementary explainable AI techniques to identify both global (nationwide) and local (state-specific) predictors of financial hardship, such as contact from debt collection agencies. We develop a machine learning model specifically suited for highly categorical, imbalanced survey data. This work delivers a scalable, regulation-compliant blueprint for early warning systems in finance, demonstrating how FL can power socially responsible AI applications in consumer credit risk and financial inclusion.

This study presents a three-step machine learning framework to predict bubbles in the S&P 500 stock market by combining financial news sentiment with macroeconomic indicators. Building on traditional econometric approaches, the proposed approach predicts bubble formation by integrating textual and quantitative data sources. In the first step, bubble periods in the S&P 500 index are identified using a right-tailed unit root test, a widely recognized real-time bubble detection method. The second step extracts sentiment features from large-scale financial news articles using natural language processing (NLP) techniques, which capture investors' expectations and behavioral patterns. In the final step, ensemble learning methods are applied to predict bubble occurrences based on high sentiment-based and macroeconomic predictors. Model performance is evaluated through k-fold cross-validation and compared against benchmark machine learning algorithms. Empirical results indicate that the proposed three-step ensemble approach significantly improves predictive accuracy and robustness, providing valuable early warning insights for investors, regulators, and policymakers in mitigating systemic financial risks.

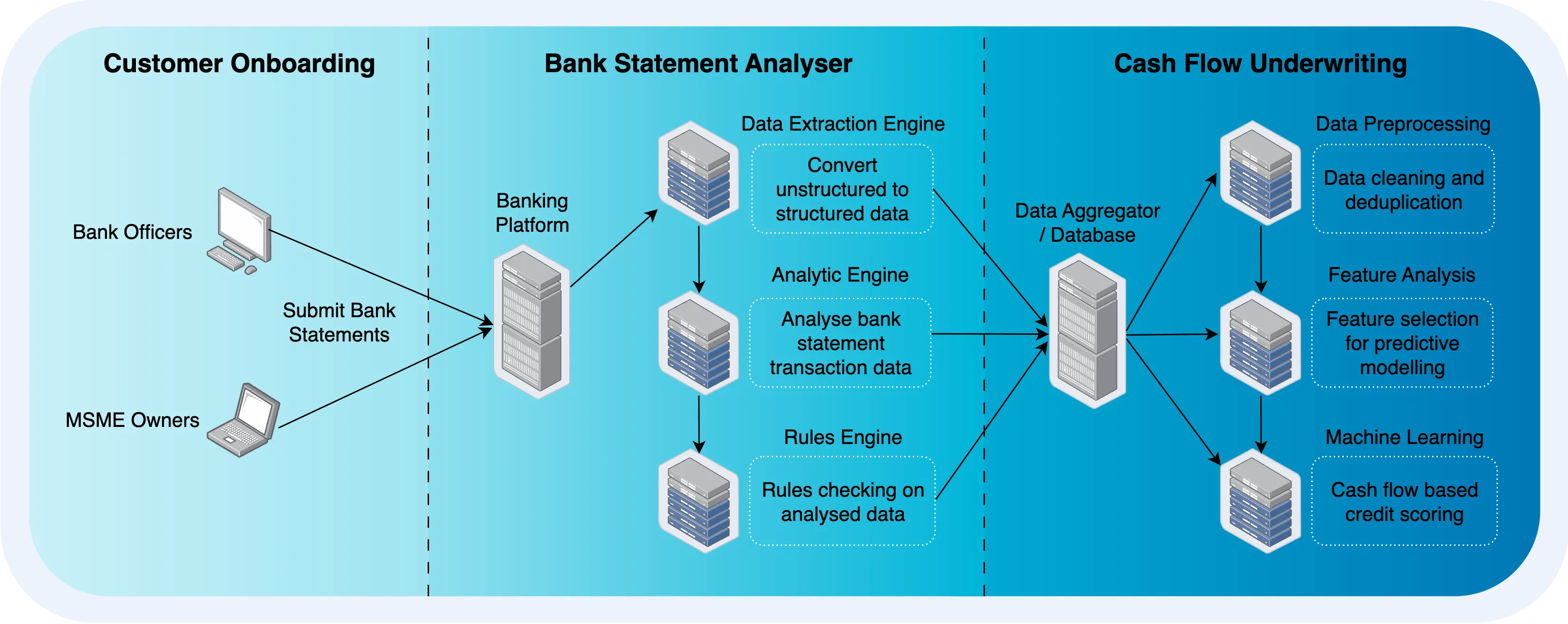

Despite accounting for 96.1% of all businesses in Malaysia, access to financing remains one of the most persistent challenges faced by Micro, Small, and Medium Enterprises (MSMEs). Newly established businesses are often excluded from formal credit markets as traditional underwriting approaches rely heavily on credit bureau data. This study investigates the potential of bank statement data as an alternative data source for credit assessment to promote financial inclusion in emerging markets. First, we propose a cash flow-based underwriting pipeline where we utilise bank statement data for end-to-end data extraction and machine learning credit scoring. Second, we introduce a novel dataset of 611 loan applicants from a Malaysian lending institution. Third, we develop and evaluate credit scoring models based on application information and bank transaction-derived features. Empirical results show that the use of such data boosts the performance of all models on our dataset, which can improve credit scoring for new-to-lending MSMEs. Finally, we will release the anonymised bank transaction dataset to facilitate further research on MSME financial inclusion within Malaysia's emerging economy.

A growing empirical literature suggests that equity-premium predictability is state dependent, with much of the forecasting power concentrated around recessionary periods \parencite{Henkel2011,DanglHalling2012,Devpura2018}. I study U.S. stock return predictability across economic regimes and document strong evidence of time-varying expected returns across both expansionary and contractionary states. I contribute in two ways. First, I introduce a state-switching predictive regression in which the market state is defined in real time using the slope of the yield curve. Relative to the standard one-state predictive regression, the state-switching specification increases both in-sample and out-of-sample performance for the set of popular predictors considered by \textcite{WelchGoyal2008}, improving the out-of-sample performance of most predictors in economically meaningful ways. Second, I propose a new aggregate predictor, the Aligned Economic Index, constructed via partial least squares (PLS). Under the state-switching model, the Aligned Economic Index exhibits statistically and economically significant predictive power in sample and out of sample, and it outperforms widely used benchmark predictors and alternative predictor-combination methods.

Time series forecasting is important in finance domain. Financial time series (TS) patterns are influenced by both short-term public opinions and medium-/long-term policy and market trends. Hence, processing multi-period inputs becomes crucial for accurate financial time series forecasting (TSF). However, current TSF models either use only single-period input, or lack customized designs for addressing multi-period characteristics. In this paper, we propose a Multi-period Learning Framework (MLF) to enhance financial TSF performance. MLF considers both TSF's accuracy and efficiency requirements. Specifically, we design three new modules to better integrate the multi-period inputs for improving accuracy: (i) Inter-period Redundancy Filtering (IRF), that removes the information redundancy between periods for accurate self-attention modeling, (ii) Learnable Weighted-average Integration (LWI), that effectively integrates multi-period forecasts, (iii) Multi-period self-Adaptive Patching (MAP), that mitigates the bias towards certain periods by setting the same number of patches across all periods. Furthermore, we propose a Patch Squeeze module to reduce the number of patches in self-attention modeling for maximized efficiency. MLF incorporates multiple inputs with varying lengths (periods) to achieve better accuracy and reduces the costs of selecting input lengths during training. The codes and datasets are available at https://github.com/Meteor-Stars/MLF.

Multifractality in time series analysis characterizes the presence of multiple scaling exponents, indicating heterogeneous temporal structures and complex dynamical behaviors beyond simple monofractal models. In the context of digital currency markets, multifractal properties arise due to the interplay of long-range temporal correlations and heavy-tailed distributions of returns, reflecting intricate market microstructure and trader interactions. Incorporating multifractal analysis into the modeling of cryptocurrency price dynamics enhances the understanding of market inefficiencies, may improve volatility forecasting and facilitate the detection of critical transitions or regime shifts. Based on the multifractal cross-correlation analysis (MFCCA) whose spacial case is the multifractal detrended fluctuation analysis (MFDFA), as the most commonly used practical tools for quantifying multifractality, in the present contribution a recently proposed method of disentangling sources of multifractality in time series was applied to the most representative instruments from the digital market. They include Bitcoin (BTC), Ethereum (ETH), decentralized exchanges (DEX) and non-fungible tokens (NFT). The results indicate the significant role of heavy tails in generating a broad multifractal spectrum. However, they also clearly demonstrate that the primary source of multifractality are temporal correlations in the series, and without them, multifractality fades out. It appears characteristic that these temporal correlations, to a large extent, do not depend on the thickness of the tails of the fluctuation distribution. These observations, made here in the context of the digital currency market, provide a further strong argument for the validity of the proposed methodology of disentangling sources of multifractality in time series.

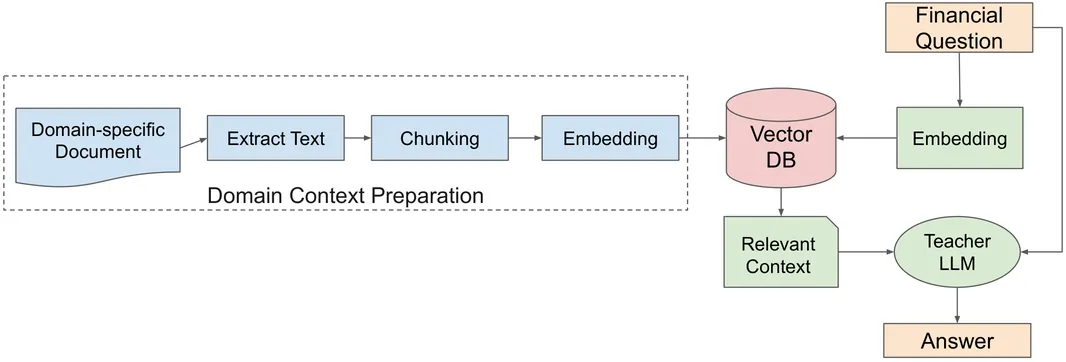

Financial analysis relies heavily on the interpretation of earnings reports to assess company performance and guide decision-making. Traditional methods for generating such analyzes require significant financial expertise and are often time-consuming. With the rapid advancement of Large Language Models (LLMs), domain-specific adaptations have emerged for financial tasks such as sentiment analysis and entity recognition. This paper introduces RAG-IT (Retrieval-Augmented Instruction Tuning), a novel framework designed to automate the generation of earnings report analysis through an LLM fine-tuned specifically for the financial domain. Our approach integrates retrieval augmentation with instruction-based fine-tuning to enhance factual accuracy, contextual relevance, and domain adaptability. We construct a sector-specific financial instruction dataset derived from semiconductor industry documents to guide the LLM adaptation to specialized financial reasoning. Using NVIDIA, AMD, and Broadcom as representative companies, our case study demonstrates that RAG-IT substantially improves a general-purpose open-source LLM and achieves performance comparable to commercial systems like GPT-3.5 on financial report generation tasks. This research highlights the potential of retrieval-augmented instruction tuning to streamline and elevate financial analysis automation, advancing the broader field of intelligent financial reporting.

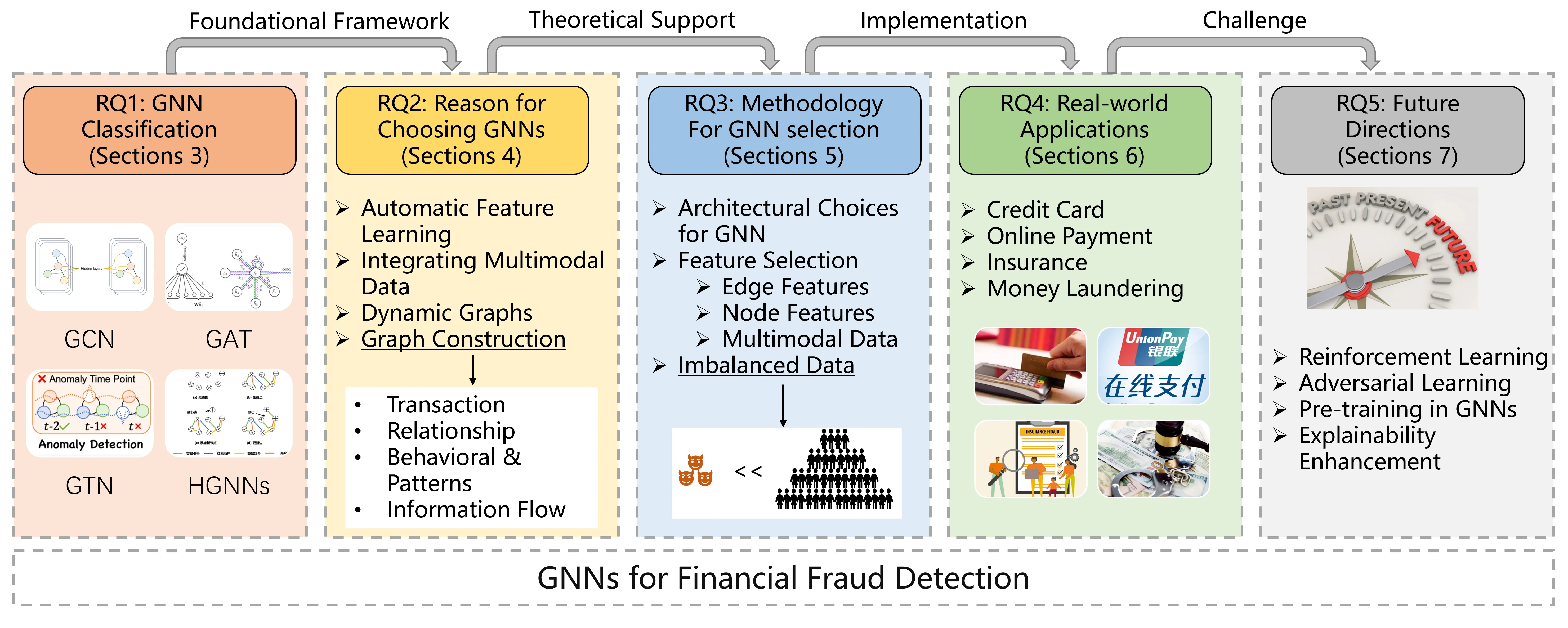

The landscape of financial transactions has grown increasingly complex due to the expansion of global economic integration and advancements in information technology. This complexity poses greater challenges in detecting and managing financial fraud. This review explores the role of Graph Neural Networks (GNNs) in addressing these challenges by proposing a unified framework that categorizes existing GNN methodologies applied to financial fraud detection. Specifically, by examining a series of detailed research questions, this review delves into the suitability of GNNs for financial fraud detection, their deployment in real-world scenarios, and the design considerations that enhance their effectiveness. This review reveals that GNNs are exceptionally adept at capturing complex relational patterns and dynamics within financial networks, significantly outperforming traditional fraud detection methods. Unlike previous surveys that often overlook the specific potentials of GNNs or address them only superficially, our review provides a comprehensive, structured analysis, distinctly focusing on the multifaceted applications and deployments of GNNs in financial fraud detection. This review not only highlights the potential of GNNs to improve fraud detection mechanisms but also identifies current gaps and outlines future research directions to enhance their deployment in financial systems. Through a structured review of over 100 studies, this review paper contributes to the understanding of GNN applications in financial fraud detection, offering insights into their adaptability and potential integration strategies.

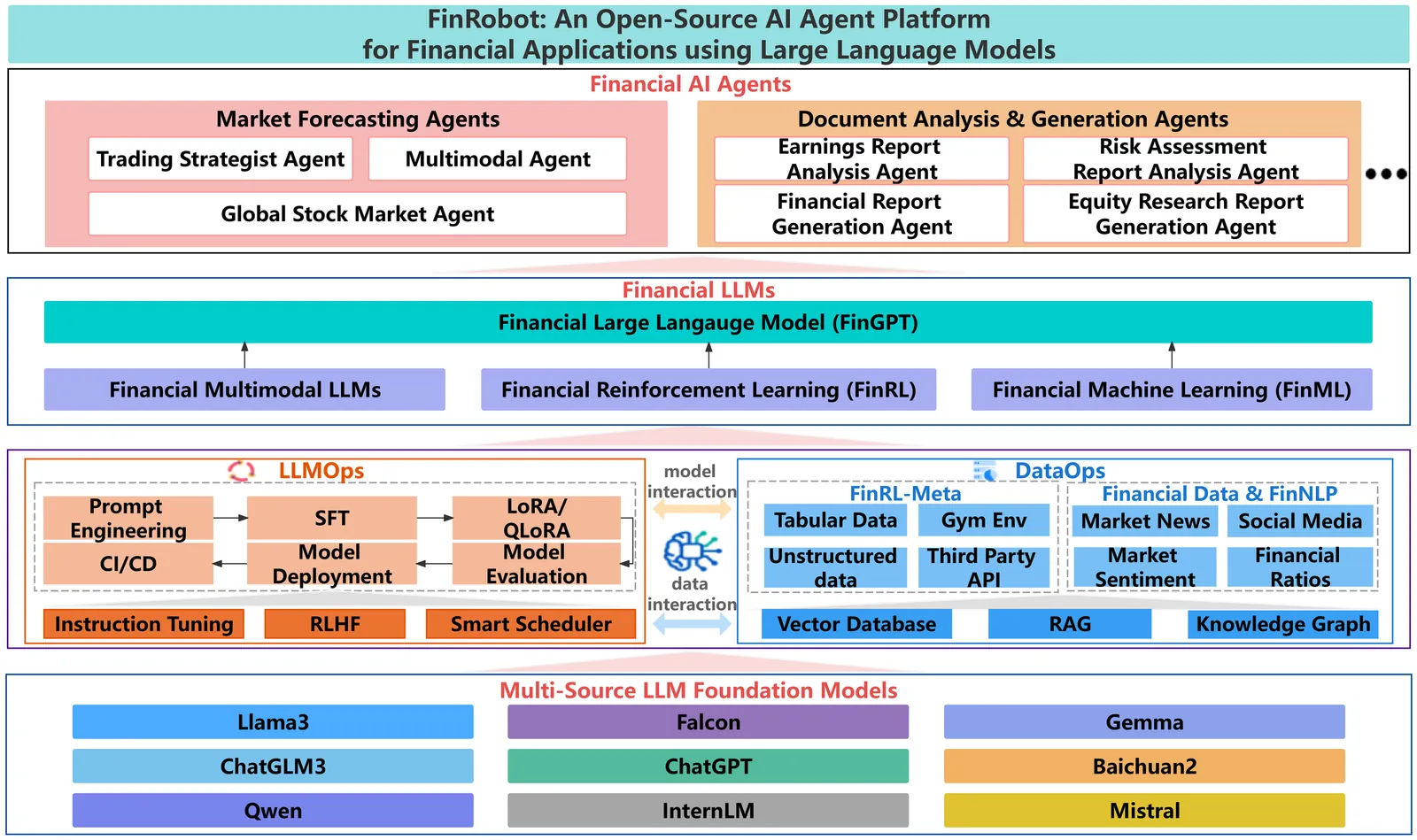

As financial institutions and professionals increasingly incorporate Large Language Models (LLMs) into their workflows, substantial barriers, including proprietary data and specialized knowledge, persist between the finance sector and the AI community. These challenges impede the AI community's ability to enhance financial tasks effectively. Acknowledging financial analysis's critical role, we aim to devise financial-specialized LLM-based toolchains and democratize access to them through open-source initiatives, promoting wider AI adoption in financial decision-making. In this paper, we introduce FinRobot, a novel open-source AI agent platform supporting multiple financially specialized AI agents, each powered by LLM. Specifically, the platform consists of four major layers: 1) the Financial AI Agents layer that formulates Financial Chain-of-Thought (CoT) by breaking sophisticated financial problems down into logical sequences; 2) the Financial LLM Algorithms layer dynamically configures appropriate model application strategies for specific tasks; 3) the LLMOps and DataOps layer produces accurate models by applying training/fine-tuning techniques and using task-relevant data; 4) the Multi-source LLM Foundation Models layer that integrates various LLMs and enables the above layers to access them directly. Finally, FinRobot provides hands-on for both professional-grade analysts and laypersons to utilize powerful AI techniques for advanced financial analysis. We open-source FinRobot at \url{https://github.com/AI4Finance-Foundation/FinRobot}.

Tail risk measures are fully determined by the distribution of the underlying loss beyond its quantile at a certain level, with Value-at-Risk, Expected Shortfall and Range Value-at-Risk being prime examples. They are induced by law-based risk measures, called their generators, evaluated on the tail distribution. This paper establishes joint identifiability and elicitability results of tail risk measures together with the corresponding quantile, provided that their generators are identifiable and elicitable, respectively. As an example, we establish the joint identifiability and elicitability of the tail expectile together with the quantile. The corresponding consistent scores constitute a novel class of weighted scores, nesting the known class of scores of Fissler and Ziegel for the Expected Shortfall together with the quantile. For statistical purposes, our results pave the way to easier model fitting for tail risk measures via regression and the generalized method of moments, but also model comparison and model validation in terms of established backtesting procedures.

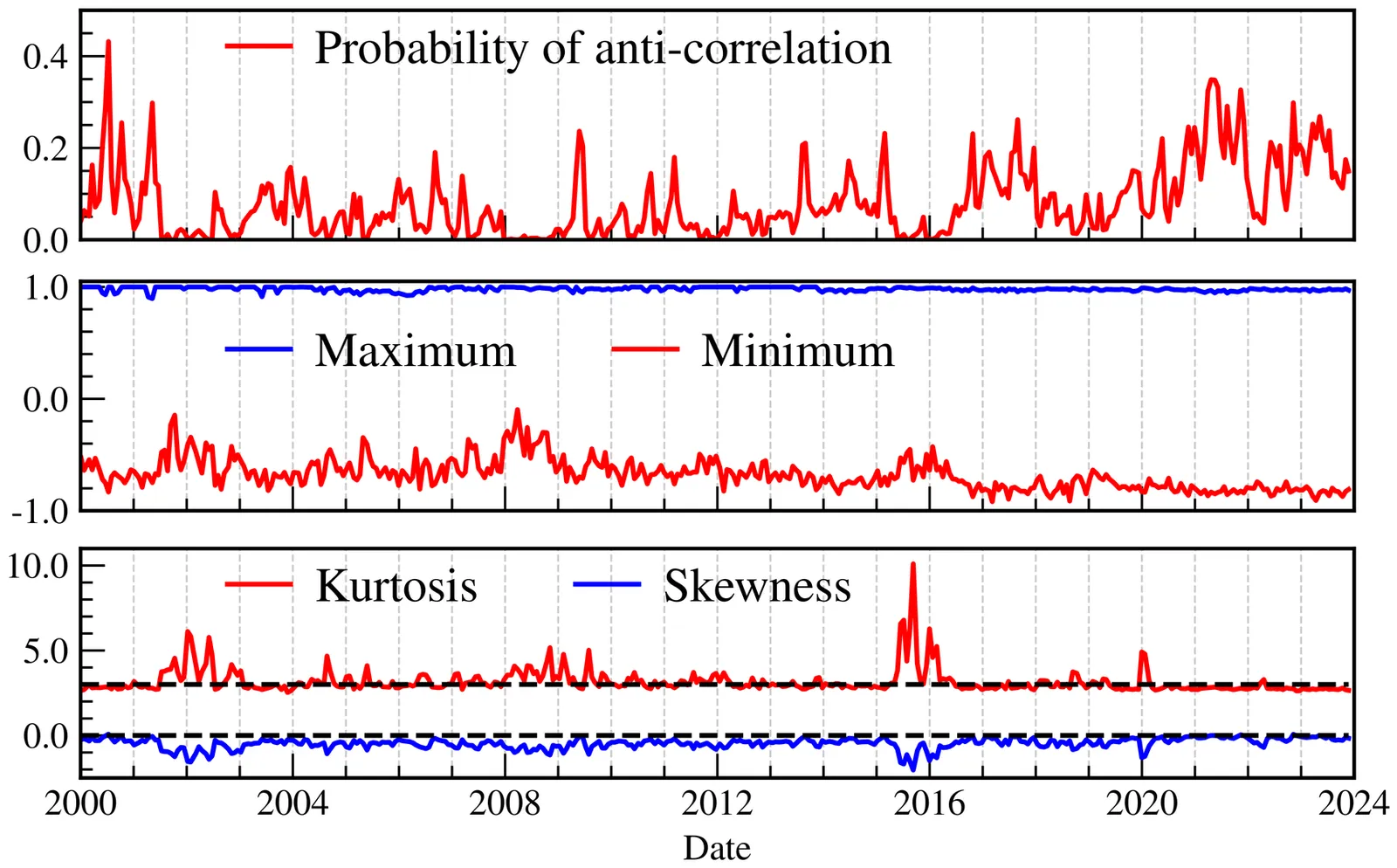

The correlation-based financial networks are studied intensively. However, previous studies ignored the importance of the anti-correlation. This paper is the first to consider the anti-correlation and positive correlation separately, and accordingly construct the weighted temporal anti-correlation and positive correlation networks among stocks listed in the Shanghai and Shenzhen stock exchanges. For both types of networks during the first 24 years of this century, fundamental topological measurements are analyzed systematically. This paper unveils some essential differences in these topological measurements between the anti-correlation and positive correlation networks. It also observes an asymmetry effect between the stock market decline and rise. The methodology proposed in this paper has the potential to reveal significant differences in the topological structure and dynamics of a complex financial system, stock behavior, investment portfolios, and risk management, offering insights that are not visible when all correlations are considered together. More importantly, this paper proposes a new direction for studying complex systems: the anti-correlation network. It is well worth reexamining previous relevant studies using this new methodology.

We propose methods to infer jumps of a semi-martingale, which describes long-term price dynamics, based on discrete, noisy, high-frequency observations. Different to the classical model of additive, centered market microstructure noise, we consider one-sided microstructure noise for order prices in a limit order book. We develop methods to estimate, locate and test for jumps using local minima of best ask quotes. We provide a local jump test and show that we can consistently estimate jump sizes and jump times. One main contribution is a global test for jumps. We establish the asymptotic properties and optimality of this test. We derive the asymptotic distribution of a maximum statistic under the null hypothesis of no jumps based on extreme value theory. We prove consistency under the alternative hypothesis. The rate of convergence for local alternatives is determined and shown to be much faster than optimal rates for the standard market microstructure noise model. This allows the identification of smaller jumps. In the process, we establish uniform consistency for spot volatility estimation under one-sided noise. Online jump detection based on the new approach is shown to achieve a speed advantage compared to standard methods applied to mid quotes. A simulation study sheds light on the finite-sample implementation and properties of the new approach and draws a comparison to a popular method for market microstructure noise. We showcase how our new approach helps to improve jump detection in an empirical analysis of intra-daily limit order book data.

Recent advancements in large language models (LLMs) have opened new pathways for many domains. However, the full potential of LLMs in financial investments remains largely untapped. There are two main challenges for typical deep learning-based methods for quantitative finance. First, they struggle to fuse textual and numerical information flexibly for stock movement prediction. Second, traditional methods lack clarity and interpretability, which impedes their application in scenarios where the justification for predictions is essential. To solve the above challenges, we propose Ploutos, a novel financial LLM framework that consists of PloutosGen and PloutosGPT. The PloutosGen contains multiple primary experts that can analyze different modal data, such as text and numbers, and provide quantitative strategies from different perspectives. Then PloutosGPT combines their insights and predictions and generates interpretable rationales. To generate accurate and faithful rationales, the training strategy of PloutosGPT leverage rearview-mirror prompting mechanism to guide GPT-4 to generate rationales, and a dynamic token weighting mechanism to finetune LLM by increasing key tokens weight. Extensive experiments show our framework outperforms the state-of-the-art methods on both prediction accuracy and interpretability.

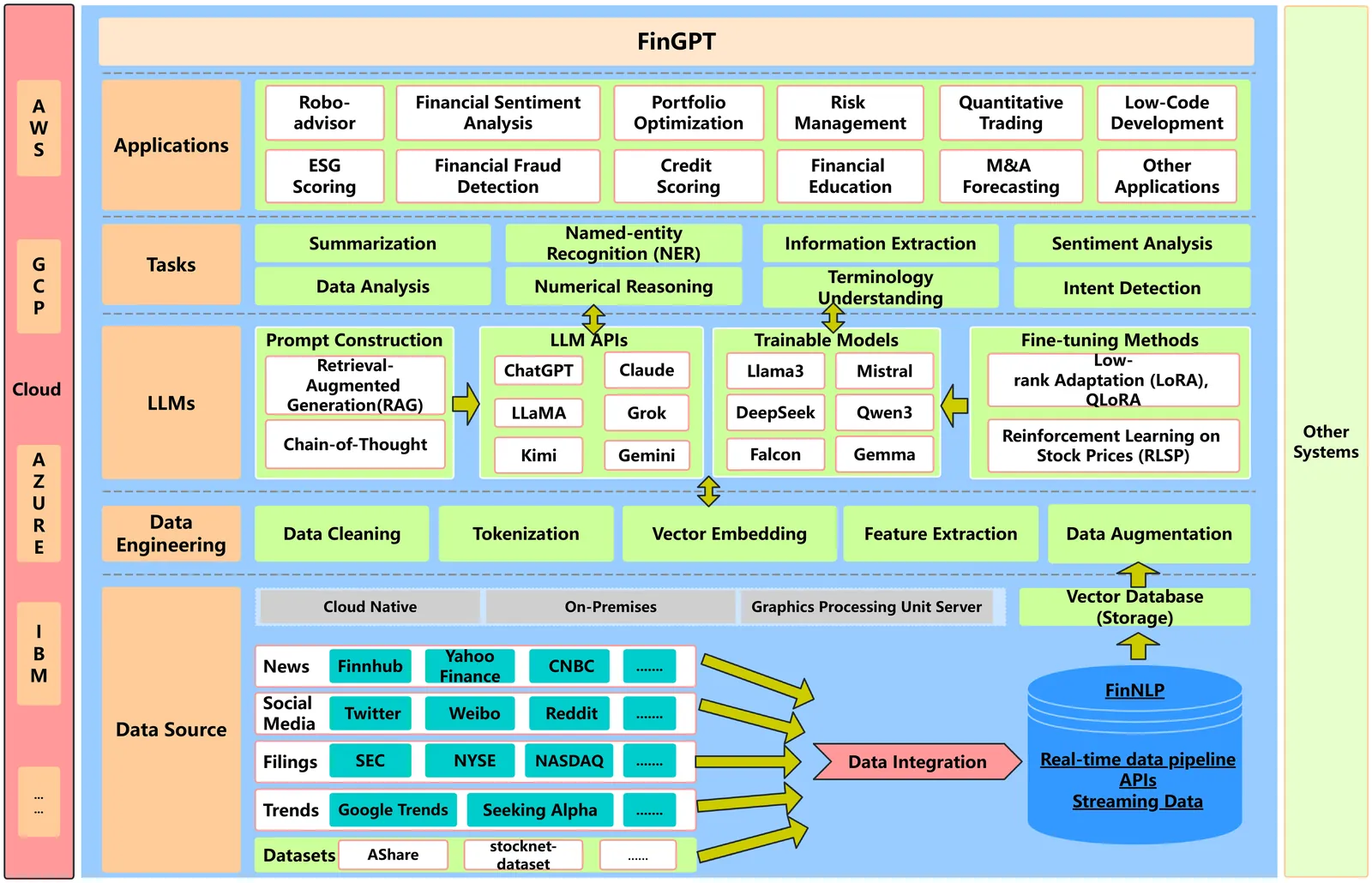

Large language models (LLMs) have shown the potential of revolutionizing natural language processing tasks in diverse domains, sparking great interest in finance. Accessing high-quality financial data is the first challenge for financial LLMs (FinLLMs). While proprietary models like BloombergGPT have taken advantage of their unique data accumulation, such privileged access calls for an open-source alternative to democratize Internet-scale financial data. In this paper, we present an open-source large language model, FinGPT, for the finance sector. Unlike proprietary models, FinGPT takes a data-centric approach, providing researchers and practitioners with accessible and transparent resources to develop their FinLLMs. We highlight the importance of an automatic data curation pipeline and the lightweight low-rank adaptation technique in building FinGPT. Furthermore, we showcase several potential applications as stepping stones for users, such as robo-advising, algorithmic trading, and low-code development. Through collaborative efforts within the open-source AI4Finance community, FinGPT aims to stimulate innovation, democratize FinLLMs, and unlock new opportunities in open finance. Two associated code repos are https://github.com/AI4Finance-Foundation/FinGPT and https://github.com/AI4Finance-Foundation/FinNLP

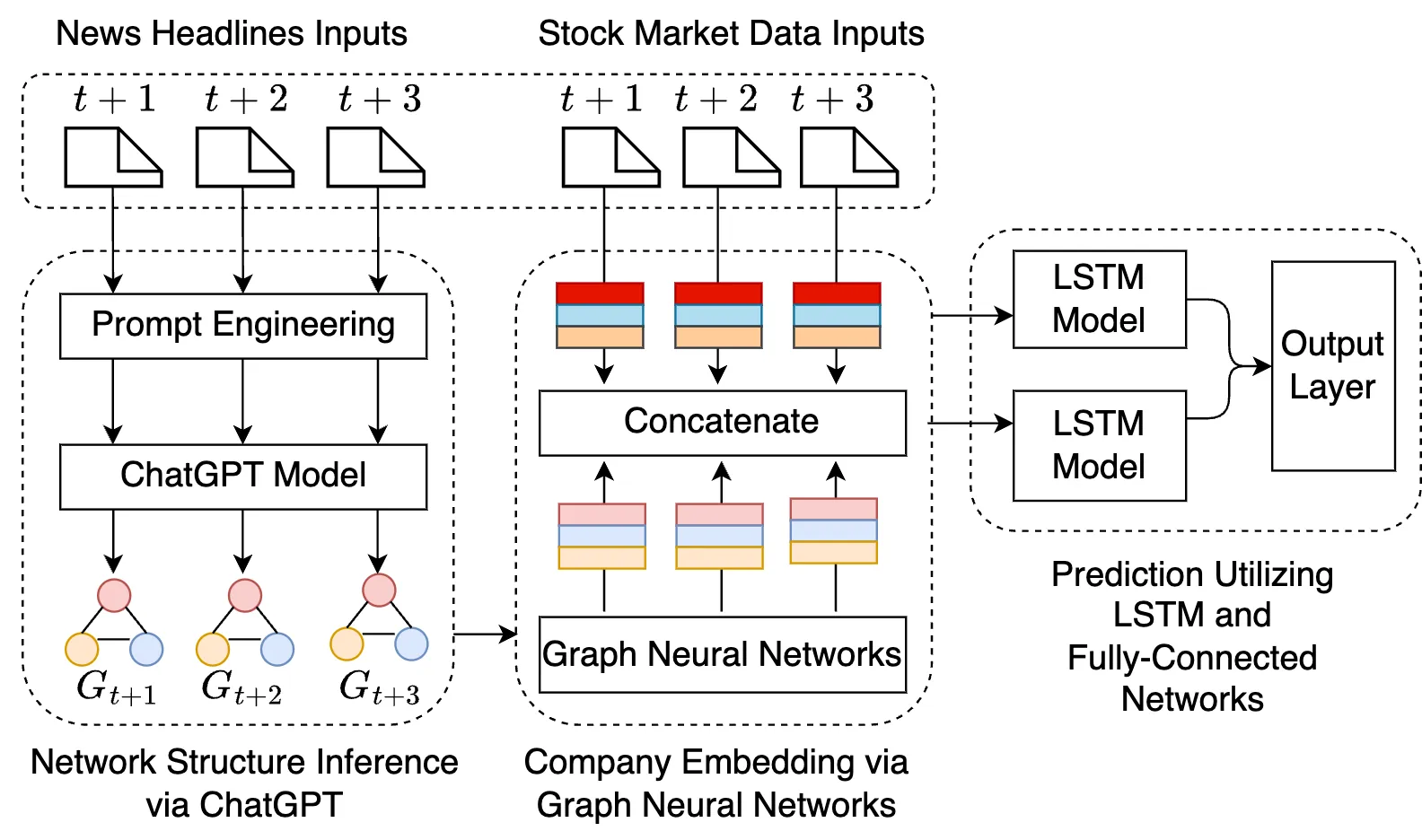

ChatGPT has demonstrated remarkable capabilities across various natural language processing (NLP) tasks. However, its potential for inferring dynamic network structures from temporal textual data, specifically financial news, remains an unexplored frontier. In this research, we introduce a novel framework that leverages ChatGPT's graph inference capabilities to enhance Graph Neural Networks (GNN). Our framework adeptly extracts evolving network structures from textual data, and incorporates these networks into graph neural networks for subsequent predictive tasks. The experimental results from stock movement forecasting indicate our model has consistently outperformed the state-of-the-art Deep Learning-based benchmarks. Furthermore, the portfolios constructed based on our model's outputs demonstrate higher annualized cumulative returns, alongside reduced volatility and maximum drawdown. This superior performance highlights the potential of ChatGPT for text-based network inferences and underscores its promising implications for the financial sector.

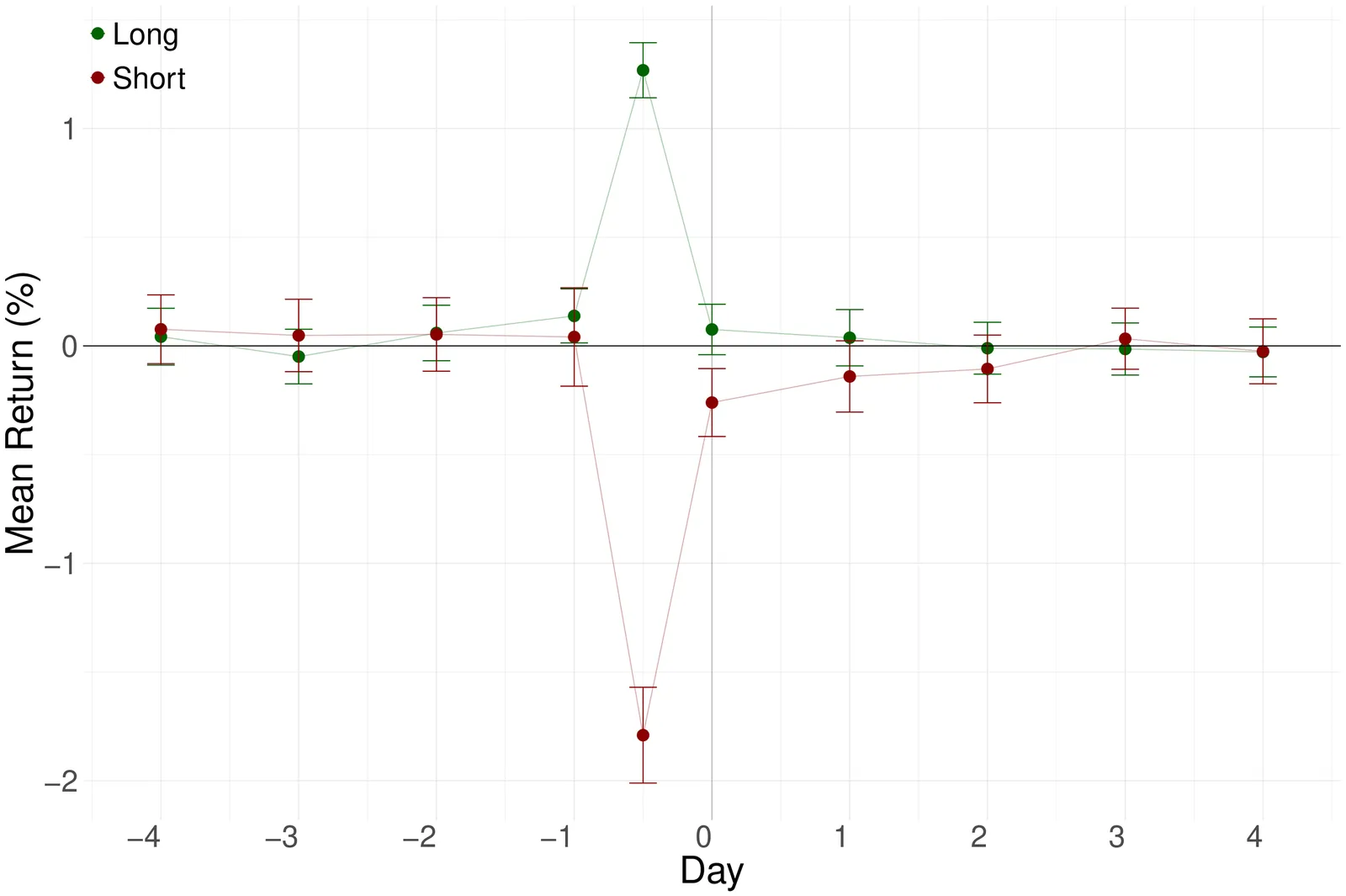

We document the capability of large language models (LLMs) like ChatGPT to predict stock market reactions from news headlines without direct financial training. Using post-knowledge-cutoff headlines, GPT-4 captures initial market responses, achieving approximately 90% portfolio-day hit rates for the non-tradable initial reaction. GPT-4 scores also significantly predict the subsequent drift, especially for small stocks and negative news. Forecasting ability generally increases with model size, suggesting that financial reasoning is an emerging capacity of complex LLMs. Strategy returns decline as LLM adoption rises, consistent with improved price efficiency. To rationalize these findings, we develop a theoretical model that incorporates LLM technology, information-processing capacity constraints, underreaction, and limits to arbitrage.

We propose a gradient-free online ensemble learning algorithm that dynamically combines forecasts from a heterogeneous set of machine learning models based on their recent predictive performance, measured by out-of-sample R-squared. The ensemble is model-agnostic, requires no gradient access, and is designed for sequential forecasting under nonstationarity. It adaptively reweights 16 constituent models-three linear benchmarks (OLS, PCR, LASSO) and thirteen nonlinear learners including Random Forests, Gradient-Boosted Trees, and a hierarchy of neural networks (NN1-NN12). We apply the framework to sector rotation, using sector-level features aggregated from firm characteristics. Empirically, sector returns are more predictable and stable than individual asset returns, making them suitable for cross-sectional forecasting. The algorithm constructs sector-specific ensembles that assign adaptive weights in a rolling-window fashion, guided by forecast accuracy. Our key theoretical result bounds the online forecast regret directly in terms of realized out-of-sample R-squared, providing an interpretable guarantee that the ensemble performs nearly as well as the best model in hindsight. Empirically, the ensemble consistently outperforms individual models, equal-weighted averages, and traditional offline ensembles, delivering higher predictive accuracy, stronger risk-adjusted returns, and robustness across macroeconomic regimes, including during the COVID-19 crisis.

Standard forecast efficiency tests interpret violations as evidence of behavioral bias. We show theoretically and empirically that rational forecasters using optimal regularization systematically violate these tests. Machine learning forecasts show near zero bias at one year horizon, but strong overreaction at two years, consistent with predictions from a model of regularization and measurement noise. We provide three complementary tests: experimental variation in regularization parameters, cross-sectional heterogeneity in firm signal quality, and quasi-experimental evidence from ML adoption around 2013. Technically trained analysts shift sharply toward overreaction post-2013. Our findings suggest reported violations may reflect statistical sophistication rather than cognitive failure.

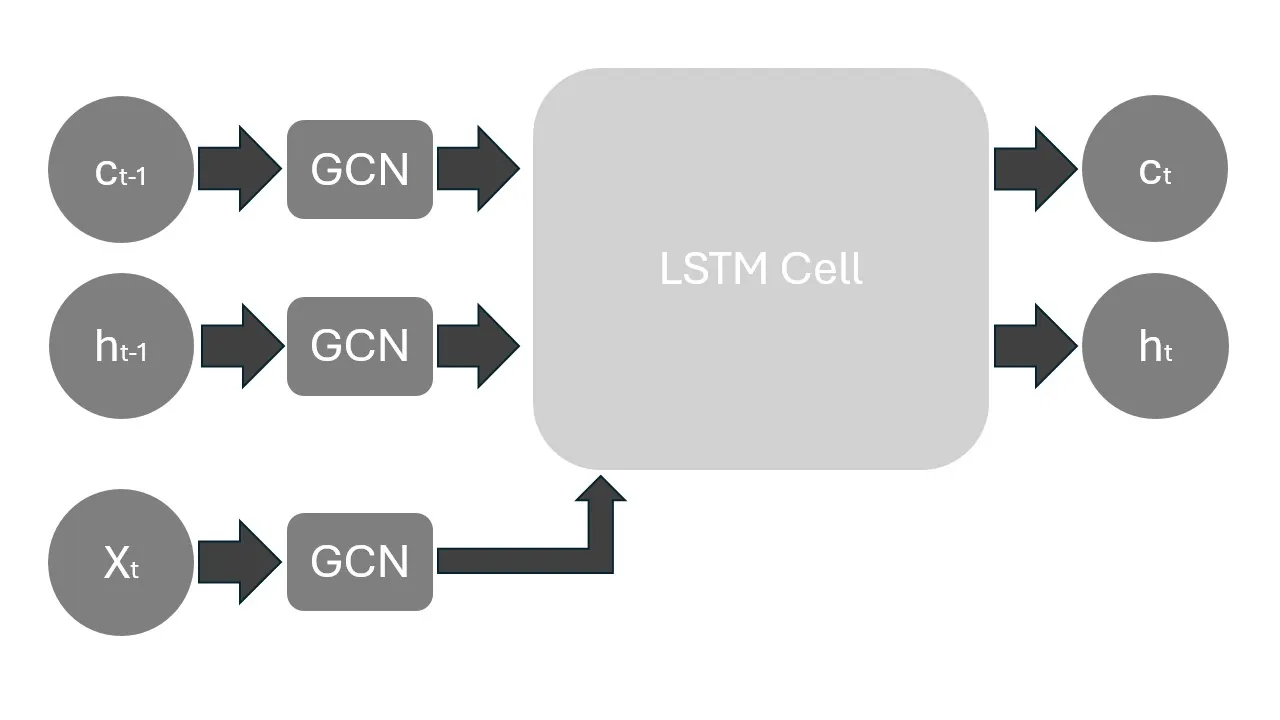

Stock return prediction is fundamental to financial decision-making, yet traditional time series models fail to capture the complex interdependencies between companies in modern markets. We propose the Full-State Graph Convolutional LSTM (FS-GCLSTM), a novel temporal graph neural network that incorporates value-chain relationships to enhance stock return forecasting. Our approach features two key innovations: First, we represent inter-firm dependencies through value-chain networks, where nodes correspond to companies and edges capture supplier-customer relationships, enabling the model to leverage information beyond historical price data. Second, FS-GCLSTM applies graph convolutions to all LSTM components - current input features, previous hidden states, and cell states - ensuring that spatial information from the value-chain network influences every aspect of the temporal update mechanism. We evaluate FS-GCLSTM on Eurostoxx 600 and S&P 500 datasets using LSEG value-chain data. While not achieving the lowest traditional prediction errors, FS-GCLSTM consistently delivers superior portfolio performance, attaining the highest annualized returns, Sharpe ratios, and Sortino ratios across both markets. Performance gains are more pronounced in the denser Eurostoxx 600 network, and robustness tests confirm stability across different input sequence lengths, demonstrating the practical value of integrating value-chain data with temporal graph neural networks.

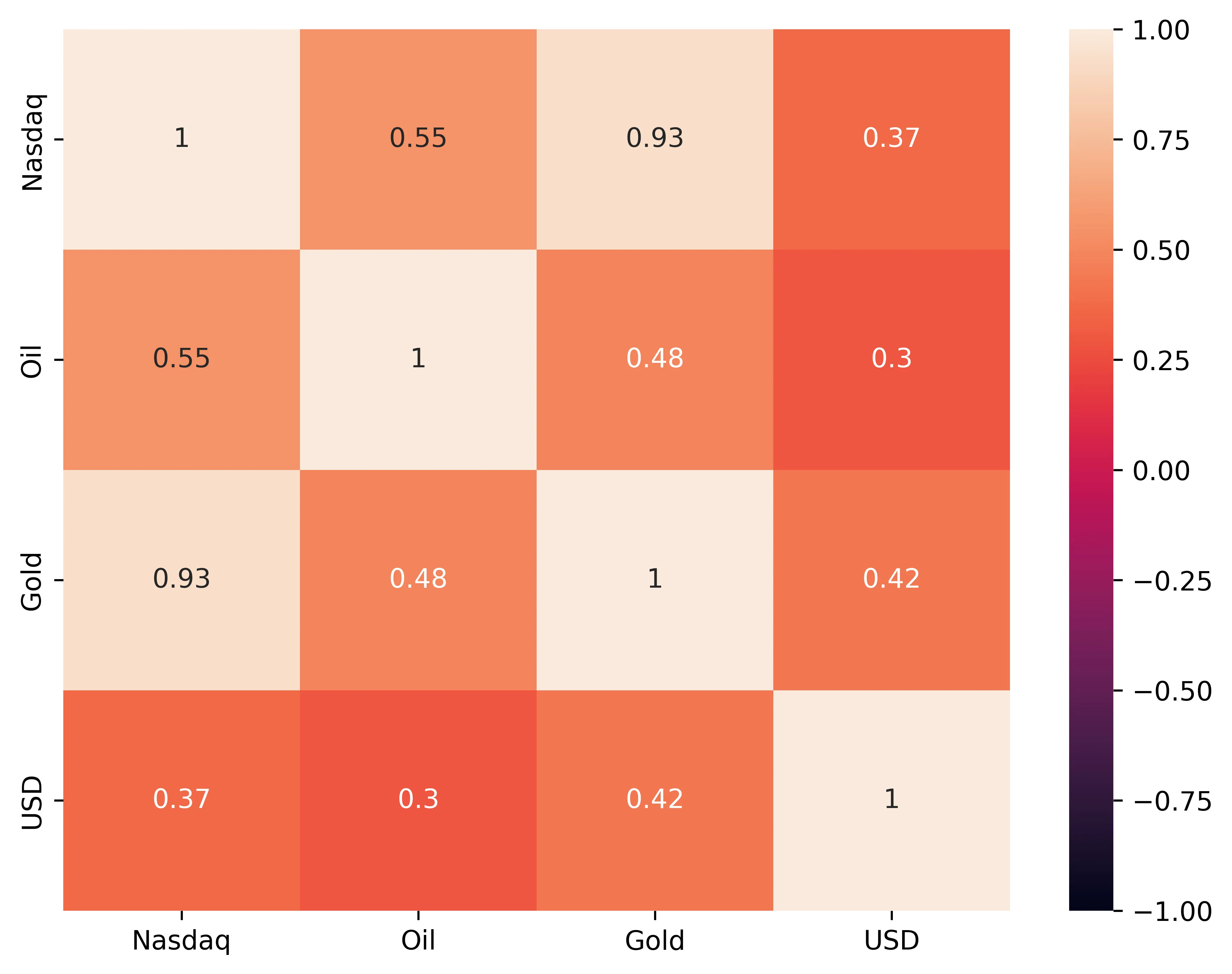

This study analyzes the dynamic interactions among the NASDAQ index, crude oil, gold, and the US dollar using a reduced-order modeling approach. Time-delay embedding and principal component analysis are employed to encode high-dimensional financial dynamics, followed by linear regression in the reduced space. Correlation and lagged regression analyses reveal heterogeneous cross-asset dependencies. Model performance, evaluated using the coefficient of determination ($R^2$), demonstrates that a limited number of principal components is sufficient to capture the dominant dynamics of each asset, with varying complexity across markets.

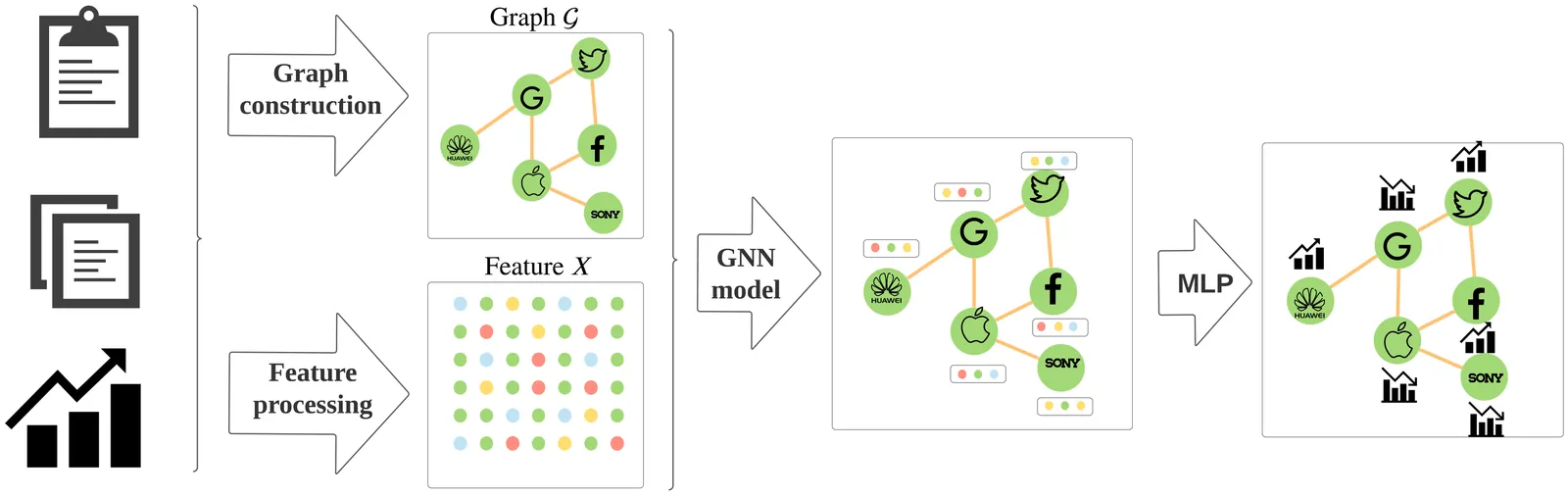

With multiple components and relations, financial data are often presented as graph data, since it could represent both the individual features and the complicated relations. Due to the complexity and volatility of the financial market, the graph constructed on the financial data is often heterogeneous or time-varying, which imposes challenges on modeling technology. Among the graph modeling technologies, graph neural network (GNN) models are able to handle the complex graph structure and achieve great performance and thus could be used to solve financial tasks. In this work, we provide a comprehensive review of GNN models in recent financial context. We first categorize the commonly-used financial graphs and summarize the feature processing step for each node. Then we summarize the GNN methodology for each graph type, application in each area, and propose some potential research areas.

We bring the theory of rough paths to the study of non-parametric statistics on streamed data. We discuss the problem of regression where the input variable is a stream of information, and the dependent response is also (potentially) a stream. A certain graded feature set of a stream, known in the rough path literature as the signature, has a universality that allows formally, linear regression to be used to characterise the functional relationship between independent explanatory variables and the conditional distribution of the dependent response. This approach, via linear regression on the signature of the stream, is almost totally general, and yet it still allows explicit computation. The grading allows truncation of the feature set and so leads to an efficient local description for streams (rough paths). In the statistical context this method offers potentially significant, even transformational dimension reduction. By way of illustration, our approach is applied to stationary time series including the familiar AR model and ARCH model. In the numerical examples we examined, our predictions achieve similar accuracy to the Gaussian Process (GP) approach with much lower computational cost especially when the sample size is large.